AEMO has released its 2026 Integrated System Plan (ISP)

The ISP identifies the Optimal Development Pathway (ODP) which AEMO expects to be the lowest-cost path to delivering reliable and secure electricity for consumers whilst supporting government policy and emissions reduction objectives to 2050.

Key highlights:

Timely investment is critical

- Timely investment in generation, storage and network infrastructure is critical and the key risk identified in the ISP to achieving the ODP.

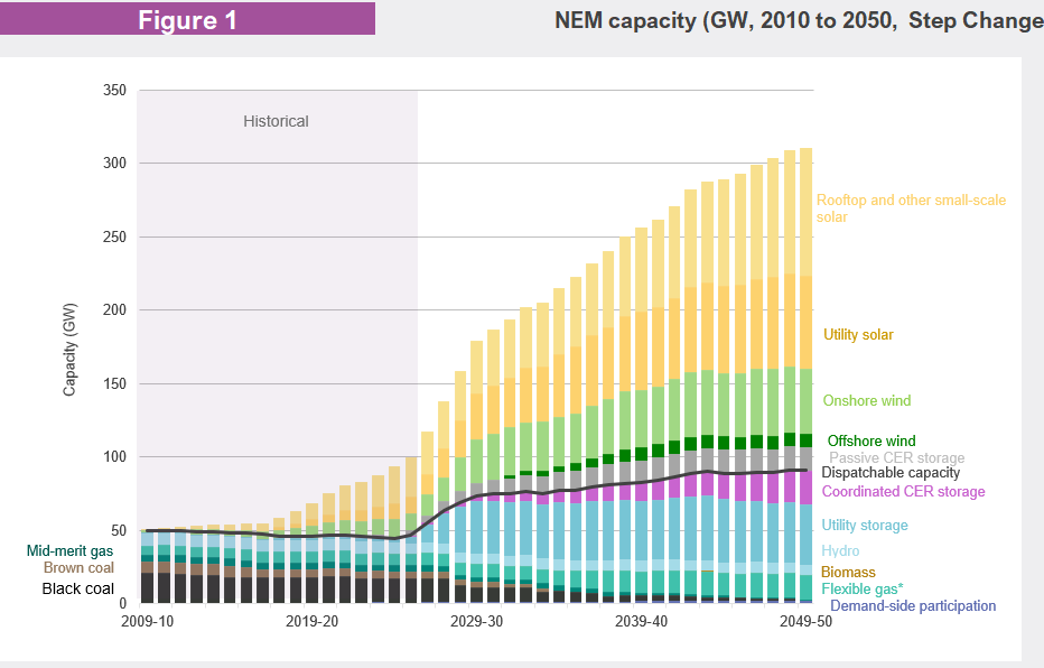

- AEMO expects $106 billion of investment to 2050 (today’s dollars) will be required under the ODP and most likely Step Change scenario.

- As a key enabler, the investment includes ~6,000km of new transmission line. This equates to around 14% extension on the existing transmission network.

Growth in CER and the exit of coal

- AEMO anticipates full retirement of coal fired generation by 2049. In its place, will be a mix of renewables firmed by batteries, pumped hydro and gas.

- Consumer Energy Resources (CER) will be a key contributor to meeting the ODP. AEMO expects 87GW in rooftop and other small-scale solar will be installed by 2050. Around two-thirds of dwellings with rooftop solar are expected to also have a battery installed by 2050, contributing 35GW. By this time, AEMO also expects 80% of vehicles to be electric.

- By 2050 and to replace coal generation, 117GW of utility-scale solar and wind (five times current levels) and almost 50GW of utility-scale dispatchable storage and hydro will be required under the ODP to meet AEMO’s forecast demand. In addition, 17GW of flexible gas-fired generation will also be required by 2050 under the ODP.

- Co-ordination and integration between Consumer and Distributed Energy Resources with the grid is highlighted as a key requirement in the ISP to meeting the ODP with distribution networks playing a key role.

Demand growth

- While the growth in CER is expected to alleviate some of the pressure on grid-scale infrastructure required, total electricity consumption across the NEM is expected to nearly double by 2050.

- Demand growth will be led by population growth, electrified processes (as consumers switch from petrol, diesel and gas to electricity), data centres and other new electricity-intensive industries.

- Recognising the uncertainties around the rapid growth in data centre demand, the ISP Step Change scenario assumes data centres will make up almost 10% of underlying demand by 2050, equivalent of around 20% of today’s grid consumption.