Edge Insights provides you with the latest news in the energy industry and showcases some of our services that help to ensure businesses maintain their optimal energy arrangements at all times. In this edition:

- Renewable projects to meet your energy needs

- State of the Market Q217

- Staff Profile: James Webster

- Government steps in to reduce gas prices

- Energy Cost Forecasts

- Raising funds for Kids’ bus

Renewable Projects Deliver Value

|

Interest in renewable generation projects has escalated on the back of elevated black and LGC prices and declining renewable offtake costs. The fulfilment of these projects presents an opportunity to change the energy supply landscape in Australia. However, will government intervention and continued downward pressure on wholesale electricity prices derail the renewable movement? Edge has worked with several renewable generation projects on development and funding applications, offtake arrangements, and firming products. Whilst ensuring that security of supply and integrity of the network is paramount, we view the progress of renewable projects as a positive step for the market and consumers. As an advisor to large Commercial & Industrial (C&I) consumers, we give careful consideration to the integration of renewable generation projects when developing procurement strategies. The advantages for both seller (generator) and buyer (C&I offtaker) make transactions of this nature mutually sought after and beneficial. In recent years, we’ve seen the cost of black energy and Large Scale Environmental Certificates (LGCs) reach all-time highs and the cost of renewable generation become increasingly competitive. |

Renewable generation projects and large C&I off-takers have never been more compatible. Our client base is dominated by large and sophisticated energy users who value proactive risk management and understand the need for diversification strategies within their portfolio. A diverse strategy may include blending spot exposure with shorter term proactive and responsive dynamic hedging strategies, and longer term aggressively priced off-take deals. These users don’t shy away from longer term propositions. A market where forward prices trade in a $5/MWh annual range with $0.20/MWh intra-day spreads are a thing of the past. Over $40/ MWh annual ranges with $5 to $10/MWh intraday spreads are the new reality. These are alarming figures. Spot prices are fundamentally higher, and we are seeing sporadic volatility that decimates quarterly averages. Market risk has escalated to levels that demand users take a more diversified and committed approach to setting prices that significantly decrease their exposure to market volatility. There is a frightening portion of aging baseload generation in the NEM. |

The current intervention by various government and jurisdictional bodies has stalled the increase in energy prices, but provides no certain longterm solution. Short-term relief will only act to delay planned projects and push prices even higher. The cycle of high prices followed by temporary relief due to intervention continues. We are helping clients beat the cycle by taking control of energy costs. We play a pivotal role in matching credible projects with suitable consumers, and give careful and considered support |

STATE OF THE MARKET

Q217 MARKET OVERVIEW

| The Federal Government’s electricity announcements continued to dominate news in the second quarter of 2017. With power prices increasing and reliability questioned following the black-out event in South Australia (SA) in March, all levels of government were keen to produce policy to assist the market. The Federal Government delivered their Energy For The Future package as part of their budget which would look at new gas development and greater gas interconnection across Australia. It also had additional funding for the Australian Competition and Consumer Commission (ACCC) and Australian Energy Regulator (AER) to conduct reviews into the market. An independent review into the future security of the national electricity market was released late in the quarter. The Finkel Review made a number of recommendations for energy security and the Federal Government has proposed to adopt 49 out of 50 of these. This includes setting up a new Energy Security Board which will be responsible for whole-ofsystem oversight for energy security and reliability. The most controversial aspect of the review was the suggestion that a Clean Energy Target be adopted if an Emissions Intensity Scheme could not be agreed. The Federal Government also announced they would restrict gas export if there was insufficient gas for domestic consumers. If a gas producer is sending more gas overseas than it is developing it must explain how it will fill any domestic shortfalls or they can be ordered to limit their export under |

You can find their other initiatives on our website. The Queensland (QLD) Government outlined their Powering Queensland Plan in June with a focus on reducing power price increases. This will be done partly by paying the distributors $770 million to reduce network costs to customers. It also reaffirmed the QLD Government’s commitment to a 50 per cent renewable target by 2030.

A reverse auction for 400 MW of renewable energy was also included. In the near term, the plan will increase system security by returning Swanbank E (385 MW gasfired generation) to service and direct Stanwell Corporation to undertake strategies to place downward pressure on wholesale prices. Full plan can be found here: https://www.dews.qld.gov.au/electricity/powering-queensland-plan The market operator (AEMO) will also look to stabilise the grid for summer 2017-18. Both South Australia and Victoria are showing lack of reserves and there is no market solution apparent at this time. In response, AEMO has triggered its Reliability and Emergency Reserve Trader (RERT) functions. AEMO will seek to build a panel of service providers who can reduce their demand at times of peak demand (or provide equivalent generation). This panel will be in place in case there are unforeseen shortfalls in the near term. For the current reserve shortfalls, AEMO is also seeking expression of interest from providers who can reduce load, benefiting the South Australian or Victorian region for summer 2017-18. |

|

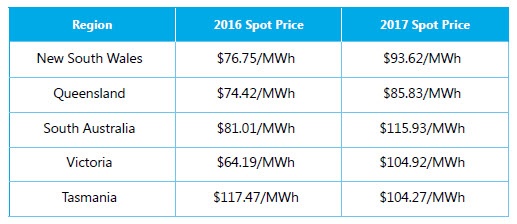

SPOT MARKETQ2 2017 was the first quarter after the Hazelwood Power Station (1,600 MW brown coal in Victoria) shut down. This had a large impact on Victoria which had an average price of $104.92/MWh compared to $64.19/MWh for Q2 2016. Spot prices were higher across all regions except for Tasmania. Tasmania was higher in 2016 primarily due to an average price in April of $236.85/MWh due to limited hydro output as Hydro Tasmania was rebuilding their storage levels. With the rain fall in May, Hydro Tasmania could continue to generate more power into the system, softening spot prices.

|

||

FORWARD CURVEThe forward curve for 2018 contracts increased with the higher spot prices. There was an additional increase when Hazelwood Power Station closed. The forward curve started reducing towards the end of the quarter due to lower spot prices. There was an additional drop when the QLD Government announced its new energy plan. It’s expected that lower QLD wholesale prices will flow through to other states. Temperatures have driven higher demand across the market, however there is still sufficient generation to meet this demand. When base load generation has been lower in Victoria, Snowy Hydro provided sufficient generation to avoid the state running out of power. |

||

STAFF PROFILE

James Webster

James Webster

What is the best piece of advice you have ever received?

“Time stands still for no-one, my son.”

Name a place you have never been to and would like to visit. Why?

Iceland. Seemingly on the edge of the world (or the Arctic Circle at least) and with a raw elemental landscape that would be awe inspiring to see.

Who or What inspires you?

As a techie and science-fiction fan, the progress being made by Elon Musk’s SpaceX amazes me. The footage of rockets landing back on earth ready to be reused is a reminder we are, at least a little bit, living in the future I imagined as a young lad.

What is one of the biggest challenges facing energy customers today?

The decision of whether to invest in battery storage is an especially challenging one; whether at the residential level, or more industrialscale capacities. The technology seems tantalising close now for the mass market, but payback periods are still significant; with the chance that an investment now may be quickly superseded by more advanced technology – at a cheaper price!

What does a typical day look like for you at Edge?

Firstly, I check all overnight data feeds have loaded correctly and automated morning reports have been distributed. After that, I am constantly designing and implementing improvements to our systems to better serve our customers.

Innovation is also an important part of my role. I develop new tools and resources for our clients to give them greater insight into their portfolios.

GOVERNMENT STEPS IN TO

REDUCE GAS PRICES

GAS EXPORTS

Earlier this quarter, the Federal Government introduced their Australian Domestic Gas Security Mechanism as a means of ensuring gas security and affordable pricing. Under this legislation, it is expected the government will have the capability to order LNG exporters to limit their exports to ensure no supply shortages in the domestic market. This action is expected to put downward pressure on prices. Regulations were due to be in place by 1 July 2017, with export restrictions to commence 1 January 2018.

GAS EXPLORATION

The government is also looking to increase new gas supply reserves by removing restrictions on exploration and development in a further push for affordability. They may face difficulty due to current restrictions imposed by individual state governments.

- Victoria (VIC) has a moratorium on both conventional and unconventional onshore gas exploration until at least 2020.

- The Northern Territory (NT) announced a moratorium on fracking of unconventional gas resources last year. This was followed by the announcement of an independent inquiry into hydraulic fracturing of onshore unconventional reservoirs.

- In 2014 New South Wales (NSW) released their Gas Plan which included a buy-back plan to purchase Petroleum Exploration Licences. Significant numbers were sold back to the government. Only one operating project remains in NSW, which is set to cease operation by 2023.

Queensland currently has no restrictions on onshore gas exploration. Their ‘Blueprint for Queensland’s LNG Industry’ didn’t include protection mechanisms for the domestic market, however they did reserve the right to set aside future gas fields for domestic supply if needed. They will release two blocks in the Surat Basin for this purpose in coming months. Gas produced from these areas will be designated for the domestic market.

GAS SPOT PRICES

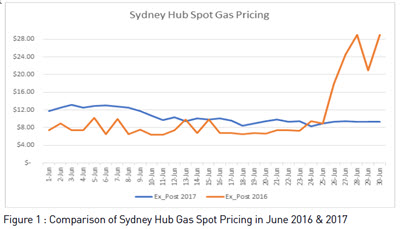

Spot Prices for the month of June have been sustained by relatively mild winter temperatures. In June 2016 the three hubs – Adelaide, Sydney and Brisbane – experienced extremely high spot prices, with Sydney trading the most expensive spot gas at $29/GJ on two separate days. Fast forward to June 2017, and on the same two days, spot gas was sold around $9.35/GJ.

FY17/18: HOW ACCURATE IS YOUR ENERGY COST FORECAST?

|

The start of a new financial year presents an opportunity to evaluate and plan your next 12 months. Energy costs represent a significant portion of operational expenditure and a forecast should be carefully considered in your plans. Energy costs can be challenging to understand for several reasons;

Things to consider when developing your forecast: Identify the data you need for reportingConsider the level of detail you require when developing your energy forecast. You may need it broken down in a number of ways; Monthly forecasts

Accurate energy budgets and forecasts rely on you transforming your historical energy data into |

Gather your informationHistorical consumption data provides a platform for future estimates. Complex organisations will require greater insight and understanding of forecast consumption. Confirm any operational changes that may impact consumption and include this in your calculation. Energy and environmental rates are especially important when forecasting in a period where your organisation is uncontracted. Incorporate marked to market pricing to avoid any surprises and prepare for any potential price shocks. This is imperative during times of volatility. Network Charges can account for up to 50 per cent of an energy invoice. These costs are regulated and need to be included in your overall forecast. Monitor progressOnce your forecast is in place, it’s important to monitor progress of actuals against forecast. Identify any significant variations and investigate. Edge provides the flexibility to develop bespoke reporting to suit your requirements. Our reporting pack includes detailed forecasts of all energy cost components.

|

RAISING FUNDS FOR KIDS’ BUS

Edge has been a long-time supporter of Nursery Road State Special School and this year, they need your help too.

The school’s 25-year-old bus is due to be decommissioned soon and $100,000 needs to be raised for a replacement. They will be holding a Spring Fair to help reach their goal for this much-needed resource.

Inclusion is vital for the students at Nursery Rd. A wheelchair accessible bus enables them to attend camps, sports programs, and participate in leisure and independent living activities in the community.

You can help by sponsoring a ride or stall at the Fair, sponsor parts of their new bus, or buy amazing artwork at the Art Auction.

All sponsors will be acknowledged on the school’s Facebook page and newsletter. If you’re considering a bigger donation, ask about signage options or advertising on the bus.

The Spring Fair is being held on Sunday 10 September at the school’s All Ability Sports Oval in Holland Park West. Donations are tax deductible and can be made by direct deposit. Contact the school on 07 3308 6333 for more information.

Full PDF edition: Edge Insights – Issue 4