Capacity Trading

As of 1 March, the new Capacity Trading Platform (CTP) and Day Ahead Auction (DAA) came online. This market arose after the Council of Australian Governments (COAG) Energy Council agreed to implement the legal and regulatory framework required to give effect to the capacity trading reform package, as recommended by the Australian Energy Market Commission (AEMC) as part of its Easter Australian Wholesale Gas Market and Pipelines Framework Review.

The reforms apply to the operators of transmission pipelines and compression facilities operating under the contract carriage model (collectively referred to as “transportation services”). The objective of the reforms is to encourage and facilitate trading of unutilised capacity on non-exempt transportation facilities. This is achieved by providing shippers with an incentive to trade spare capacity on a secondary capacity market (the CTP). If a shipper fails to sell any spare capacity prior to the nomination cut-off time, then its contracted but unnominated (CBU) capacity is then offered to other participants in an auction conducted a day ahead of the gas day (the DAA). In contrast to trades conducted by shippers prior to nomination cut-off time, the proceeds from the auction are retained by the service provider, which incentivises shippers to sell their spare capacity ahead of nomination cut-off time. (AEMO, Pipeline Capacity Trading: Overview, 2018).

According to the Australian Energy Regulator (AER) in the first two weeks of the DAA, 1.87 PJ of capacity was bought across multiple pipelines and compressors (Australian Energy Regulator, Gas Market Report, March 2019).

C&I Gas pricing

C&I gas contracts continues to be an opaque market. Contract prices have softened since the peak in 2016, however remain high and continue to put businesses under strain who are challenged with either absorbing higher costs or passing these onto customers.

AEMO recently released their Gas Statement Of Opportunity which reinforced the situation that domestic gas supply and demand balance is tight. AEMO highlighted that:

“Supply from existing and committed gas developments is forecast to provide adequate supply to meet gas demands until 2023. However, risks remain that any weather-driven variances in consumption or electricity market activity could increase gas demand, creating potential peak-day shortages as outlined in AEMO’s 2019 Victorian Gas Planning Report”.

Weather driven variances in consumption were observed in late January this year when the Cumulative Price Threshold was met and the Administered Price was activated VIC and SA. This highlight from AEMO is generally concerning as it suggests that there is unlikely to be any reprieve in gas prices in the near to medium term.

Recently, pricing for C&I customers has been observed between $11.00/GJ and $14.00/GJ subject to terms and conditions. Customers are increasingly looking at taking on more responsibility for their consumption in an effort to bring down the commodity price.

Gas Powered Generation

Gas powered generation in Q119 was 4% higher than Q118 with less generation from hydro, black coal and brown coal. There was a material increase in generation from solar and wind resources which was to be expected.

Average prices in the STTM hubs and the VIC gas market all increased in Q119 relative to Q118. Volumes were lower in the STTM markets, whereas the volumes increased through the VIC market. Gas fired generation in VIC averaged 75TJ/day in Q119, which was 23TJ/day higher than Q118. Less generation from brown coal and hydro generators was the primary driver behind this.

Regional analysis

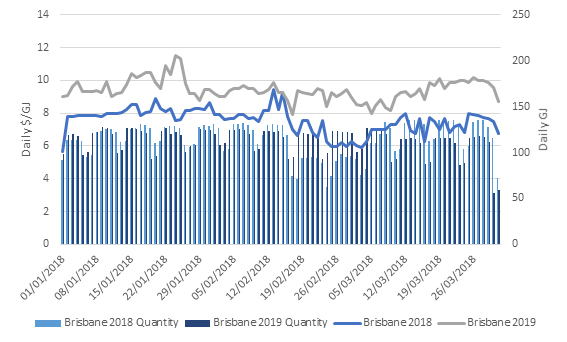

Brisbane

Brisbane STTM gas prices were higher in Q119 relative to Q118. Prices were consistently higher and generally followed a similar pricing trend. Volumes exchanged through the STTM were marginally higher in Q118 relative to Q119.

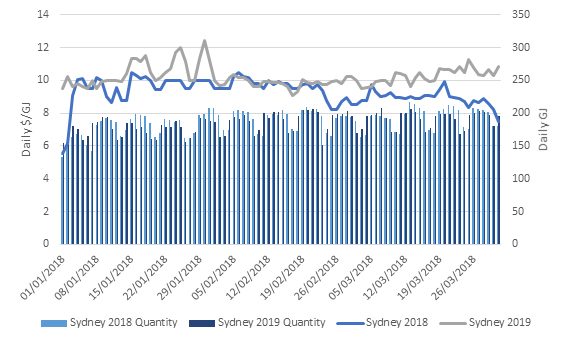

Sydney

Sydney STTM gas prices were higher in Q119 relative to Q118 with a divergence in prices in the final week of the month. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

Adelaide

Adelaide STTM gas prices were higher in Q119 relative to Q118. Q119 prices were consistently above that of Q118, with the exception of a few days at the beginning of February. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

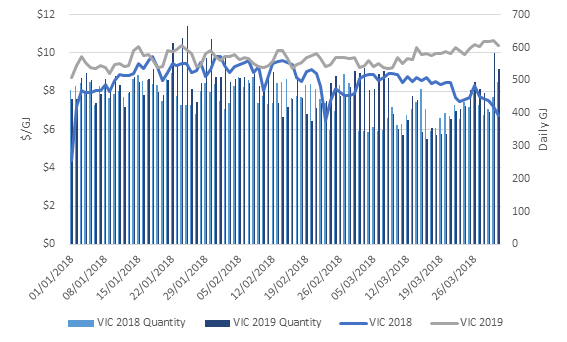

Victoria

VIC gas prices were higher in Q119 relative to Q118 with prices diverging in the final weeks of the quarter. Unlike the STTM markets, there was more volume traded through the VIC market in Q119 relative to that of Q118. On the 24th and 25th of January, there was a spike in gas volumes which was driven by higher demand from the Gas Powered Generators as a result of very high electricity prices.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220.