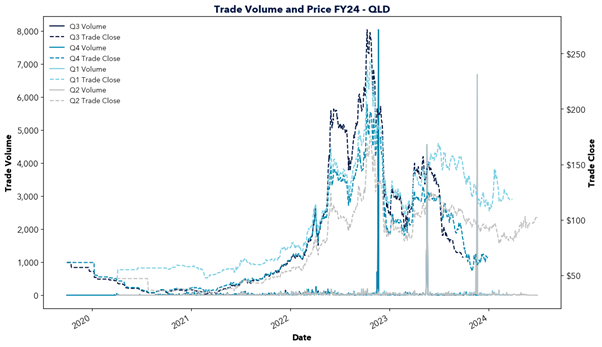

Queensland set a new record for operational demand on January 22, 2025, exactly one year after the previous record on January 22, 2024. The demand reached 11,144 MW, surpassing last year’s record of 11,005 MW.

This high demand was driven by extreme heat and associated cooling loads, significantly exceeding forecasts. Evening demand surpassed the 10% Probability of Exceedance (POE10) forecast of approximately 10.7 GW by about 0.5 GW. Similar to last year, the POE10 forecast underestimated demand, then by about 0.3–0.4 GW.

The unexpectedly high demand strained the Queensland grid, causing significant market volatility. The daily average electricity price spiked to $1,133/MWh, increasing the Q1 2025 quarterly average by approximately $45/MWh.

The situation was exacerbated by the Gladstone 2 unit tripping just before 7 PM, although it returned to service around 1 AM the next morning. Limited interconnector flows from New South Wales into Queensland, caused by constraints and ongoing issues at Bayswater 2, further compounded the problem.

Queensland is expected to see softer electricity demand in the coming week as temperatures are forecasted to decrease.

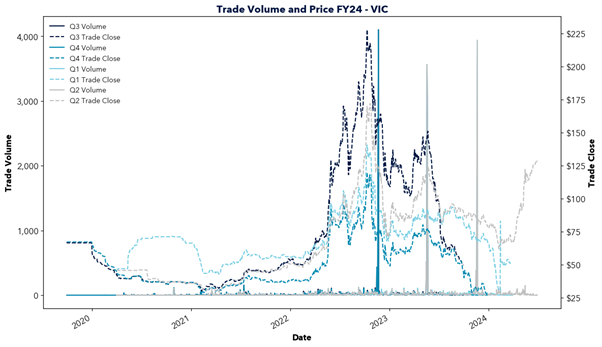

In contrast, New South Wales’ POE10 forecast is 12.8 GW tonight, driven by high temperatures across the state. While current pre-dispatch prices remain soft, such high demand means any outages or constraints could significantly impact spot prices and cause volatility.

As demand continues to rise year-on-year, concerns about supply adequacy during the energy transition are growing. Are these trends and risks adequately accounted for in future forecasts? Will supply keep pace with demand?

Looking ahead, could February 2025 bring further record-breaking demand events?