Infigen have submitted a letter to the Australian Energy Market Commission’s Chairman requesting the introduction of an Operating Reserves and Fast Frequency Response rule change. Infigen state in their letter that this market proposal they have put forward would “relatively simple to implement and would provide added confidence that sufficient resources to respond to unexpected changes in supply or demand would be available”, as stated in their letter.

Most importantly, Infigen have stated a rule change such as this would remove the reliance on and provide an alternative to the RERT (Reliability and Emergency Response Trader) procurement and contracts of which cost consumers $34.5 million, and avoid further intervention in the market by the market operator. Infigen believe that a “free-rider” problem may occur under tight capacity scenarios in the market increased risks of random government interventions to avoid adverse market and operational outcomes.

As such, they believe “marginal value of incremental capacity is by definition very high and delivers considerable benefits to the entire market’” calling out that raising the market price cap does not solve the issue with systemic risk to portfolios/participants caught short due to plant outages or network failures. Instead, Infigen have called for the introduction of a Operating Reserves market for near term to avoid increasing the market price cap and increase the reliability and security of supply to consumers.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

On the 26 March 2020, the energy market bodies including the Australian Energy Market Commission (AEMC), Australian Energy Market Operator (AEMO) and the Australian Energy Regulator (AER) wrote a letter to the Australian Federal Government’s Energy Minister, Angus Taylor which advised and sought for the consideration to consider a longer implementation time-frame for the market’s transition to the 5 minute settlement regime which was pegged to begin on 1 July 2021.

The Market bodies have stipulated the reasoning for this is due to the vast impacts to industry and the workforce that have occurred due to the COVID-19 outbreak. The letter to Mr Taylor proposes delaying the start date of 5 minute settlement by 12 months so industry can defer further/remaining expenses associated with preparing for 5 minute settlement.

It also states that AEMO will still work to the same deadline, albeit 12 months would provide AEMO with extra time to ensure 5 minute scheduling and dispatching engines are sound at least in a development environment. As yet we do not know if the 5 minute settlement will get the go ahead to be delayed, with market bodies still reaching out to market participants to advise as to whether this will be advantageous or not.

The impact of a 5 minute settlement delay to the market will be impact all participants and investment decisions, there are some calling out this only extends coal-fired generation’s life-span, but if you have been watching the futures prices and spot prices of late, coal-fired generation is already in a world of hurt with no doubt a lot of questions being raised about the remaining lifespan of some coal plant in both QLD and NSW. Should 5 minute settlement be delayed by 12 months, there is the likelihood we see the slide of investment in some fast start plant, such as new batteries and hydro.

Gas-fired generators who have not re-tuned/upgraded their synchronising and start time to less than 5 minutes will still have the 30 minute settlement price to fall back on at least for another 12 months and be able to capture any value the 30 minute average settlement price may represent. The flip side of 5 minute settlement is that it would be very good for renewable generation as it would make the thermal plat operators reassess their operating philosophies with gas likely more removed from the market, and propping up the price.

The 2021/2022 financial year was likely to be a more costly financial year given the introduction of 5 minute settlement, which would effectively mean a vast majority of gas plant would not be able to curb price spikes as effectively under the new settlement regime, resulting in a change to their operating philosophy, however both the impacts of COVID-19 an the recent oil price collapse has significantly changed this stance.

Unfortunately, there is no real way to know how much of an impact globally it will have, and how long the impacts of COVID-19 will last. Similarly, with Saudi-Arabia and Russia both engaged in a price/supply war over Oil (two of the largest producers of oil) it is all hard to depict how long the extremely cheap domestic gas prices will last, particularly with investment decisions in new domestic gas likely put on hold.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

COVID-19 has impacted us all in recent weeks. At Edge we

have put plans in place that have allowed us to provide all services our clients

require without disruption.

We are working diligently to understand the impacts COVID-19

could have on the energy markets in the short and longer term. As more

information comes to light, we will provide further updates on the impacts to

the market and our clients.

As we are only a few weeks into this pandemic we will try

and provide an understanding of the impact COVID-19 could have on the market.

Oxford economics, a team of 250 economists, has recently

published a paper providing a high-level update on the impact of the pandemic

on the world economy. Their initial work predicts a short, sharp recession to

the global economy with major national economies going into deep recession

during the first half of 2020. It is modelled that over the full year global

growth will drop to zero.

Oxford economics are predicting, based on historic experience,

a strong bounce back in activity once social distancing measures are relaxed.

It is forecast that businesses that can get through the first half of 2020

should be prepared for a strong second half of 2020, with global growth forecast

above 4%.

Overseas experience

As China was the first country to close-down as a result of

COVID-19 we can learn from their recent energy experience and translate it into

the Australian market.

In January and February energy production dropped

significantly with thermal power dropping 8.9%, hydro dropping 11.9% and nuclear

and wind dropping to a lesser extent at 2.2% and 0.2% respectively. On the flip

side Solar generation increase by 12%.

Early indications are that thermal and hydro station dropped

production the most due to reduced staffing level causing lower operational

hours. Renewables were impacted the least due to their non-dispatchability.

It is estimated that during the height of the Chinese

lockdown period over the 27 days, demand decreased by 16%.

At Home in Australia

Generation

Large generation portfolio’s including the likes of Stanwell

and AGL have publicly acknowledged they have put plans in place to ensure

generation meets demand, this includes stockpiling coal to ensure security of

fuel supply. Smaller generators on the other hand may not have the staff to

guarantee operation of their units over the long term due to illness.

Energy Price Impacts

With the additional impact of lower energy demand in Asian countries such as China, Australia’s liquefied natural gas demand significantly reduced, resulting in excess domestic gas supply particularly on the east coast of Australia. Although majority of the LNG facilities on the east coast reside in QLD, we have seen an increase in gas generation and a decrease in bid prices in regions more dependent on and abundant with gas-fired generation, such as South Australia. We are seeing approximately 600 MW more of gas-fired generation in March 2020, compared to March 2019, bid in at prices below $50/MWh. Assisting this is the collapse in natural gas prices in the Adelaide Short-term Trading Market, which has traded at the mid to high $5/GJ range for March 2020, compared to the significantly higher price range of $10 – $11/GJ we witnessed back in March 2019. Both of these variables are introducing cheaper supply in the energy markets both for heating (in homes) and electricity generation. With interconnection remaining relatively unconstrained this is resulting in lower prices across all NEM regions.

AEMO

AEMO has put in place its pandemic response plan so the

market operator can continue to operate the NEM and WEM efficiently and safely.

Key actions in the pandemic plan include limiting contact with key staff such

as control room and other business critical staff.

Demand

Following the initial breakout of COVID-19 in Australia and

the early shutdown of some businesses, demand fell by about 600MW in NSW or

about 8% of average demand. This was reflective of all states. Over the recent

week the steep reductions in demand experienced at the start of COVID-19 have

flattened out as a result of two possible reasons. In some regions such as

Victoria, demand has increased. The first reason for this change in demand is

consumption has moved from businesses to individual homes. Across Australia average

demand is currently only 7% below last month’s average. The demand change is

also attributed to seasonal change which has resulted in a reduction in load

associated with cooling.

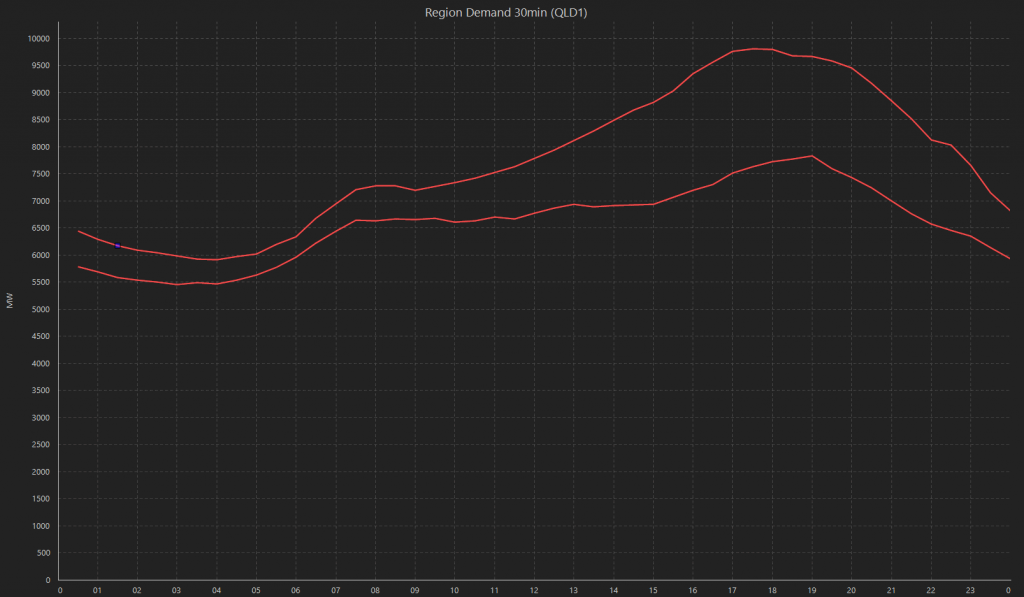

Change in demand – daily profile

The chart below illustrates the change in demand across the

day and compares a summer profile and a transition to an autumn profile. The

top line is early February with the bottom-line showing demand from Monday the

23rd March.

Source: AEMO 2020

The chart shows morning peak has reduced slightly however the demand over the evening peak has dropped significantly.

Impact of large users

It is expected that large users would be impacted significantly

by the virus however this does not appear to be the case. With parts of the

world such as South Africa shutting down mines and industry following

government direction the supply / demand balance is falling in the favour of

Australia. Add to this the favourable exchange rates, the export potential of

commodities from Australia remains strong. The Australian mining industry is

also designated as an ‘Essential Service’ so at this stage they are sheltered

from future lock downs. This positive news for the mining sector which will

benefit mining rich states with demand expected to reduce to a lesser extent

than other states.

Renewables

If the trends overseas are reflected in Australia the

current installed capacity of renewable generation will continue to operate at

strong levels providing staffing is available to operate and control the

assets.

There will be a likely slowdown in the development of

renewable projects as a result of the restrictions on travel, meetings and

specialist staff available for construction, connection, commissioning and

final approvals.

This slowdown will impact the future mix of generation

assets across Australia, the current trend in carbon emission reductions and

the supply and price of environmental products.

LGCs

Edge has modelled the impact of a 10% reduction in demand

with a business as usual generation profile for large scale renewable generators

to understand the impact this downturn may have on LGC supply and price.

The 10% reduction in demand could reduce the RPP percentage

by 0.32%. The likely effect of a reduced percentage and business as usual

renewable production will be surplus LGCs in the short term and reduced prices

for LGCs.

STCs

With the downturn of the economy it is expected that less

roof top solar will be installed resulting in a reduction in the current

surplus of certificates carried forward since 2017. The reduction is expected

to reduce the STP below 20%.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

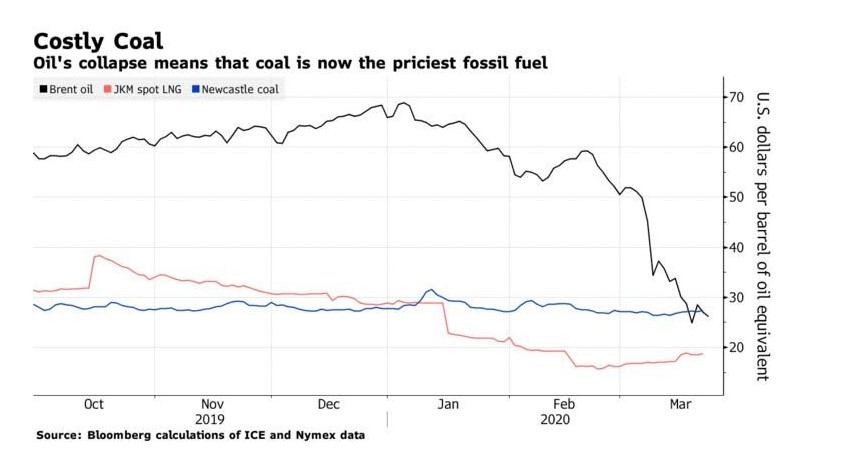

We have all seen recently the impact that COVID-19 has had on global markets, in terms of stock prices, equity markets and of commodity markets.

Exacerbating this was the poor timing of Saudi Arabia and Russia’s spat over oil prices and both choosing to disagree on production levels, the disagreement lead to Saudi Arabia choosing to flood the oil markets with supply inevitably driving oil prices down significantly, with the WTI Crude Oil index reaching its lowest point in the last 5 plus years or so, trading in the low to mid $USD 20/barrel, also impacting the Brent Crude Oil index, which fell to its lowest point in the last 5 years or so to prices of the high $USD 20/barrel. Both events have lead to something quite astounding, with Bloomberg Green on the 23rd of March 2020 calculating that coal was officially the world’s most expensive fossil fuel.

Source: Bloomberg Green – Bloomberg 2020

This does not come as a huge surprise when the oil price has tanked off the back of a trade war between Saudi Araba and Russia, two of the largest producers of oil in the world. Additionally, international gas prices have also tanked with majority of long-term gas deals linked to an oil price index (likely Brent Crude) and the Japan Korea Marker – a major LNG (liquefied natural gas) index for Asia also falling with a supply glut due to reductions in demand from some of the largest demand centres such as China who went into a full lockdown earlier this year due to COVID-19.

According to Bloomberg calculations (Bloomberg 2020), the significant fall from grace in oil prices has meant that global crude benchmark is now priced below the Australian Newcastle coal index, which sat at $66.85 a metric ton on ICE Futures Europe on the 23/03, equivalent to $27.36 per barrel of oil with Brent futures that day ending at $26.98 per barrel.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The South Australian (SA) region has been separated from the remainder of the NEM regions due to the destruction of the main alternating-current (AC) interconnector between SA and Victoria (VIC).

What occurred:

On the 31st of January 2020 during wild storms that lashed eastern SA, western VIC, the 500kV main (AC) interconnection cable running through southwestern VIC was disconnected due to transmissions towers east of Heywood (Victoria) and west of Geelong (Victoria) collapsing in damaging storms and extremely strong winds.

When this occurred,

Interconnection flows quickly swung from exporting MW’s into VIC, to importing MW’s into SA.

Alcoa’s Portland aluminium smelter tripped which only exacerbated the problem,

A handful of wind farms were cut off from the market including McCarthur Wind Farm (420 MW) in Victoria, and the three Lake Bonney Projects in South Australian (~278.5 MW)

What does this mean:

Basically SA has been left to fend for itself, cut-off from the rest of the NEM

All MW’s (majority of all, with the small Murraylink direct-current interconnector still available) and frequency control services must be sourced from SA, locally.

Currently all SA generators are running hard and optimising portfolio’s for frequency control services (FCAS) prices rather than regional reference prices (spot price)

Additionally, a vast majority of gas-fired generation units including, Osbourne GT, Pelican Point, Torrens Island A and B units have and continue to receive market intervention notices from AEMO requiring them to be online

This is adding to the oversupply in the region with wind generation quite strong for this time of the year,

Not to mention, the wind generation, being a variable generation type, is not helping from a forecast perspective for AEMO, adding to the FCAS costs and requirements in the SA region.

Solution:

AEMO have indicatively provided a two week return time off the back of AusNet’s (interconnector owner) initial assessment and action plan to fix the interconnector.

AusNet’s solution is to construct temporary interconnection with power poles and lines to have arrived on site yesterday (03/02/2020).

Current weather forecast and impact on spot price:

Currently temperatures are set to be relatively mild for an SA summer at this stage.

However, temperatures are expected to reach the late 20’s and early 30’s towards the end of the week, historically, temperatures at these levels have encouraged higher demand and the need for imports from VIC, which will not be possible with the largest interconnector between the two regions out of action.

Although we are seeing some extreme lows in spot price, there is the possibility we could see some extreme highs. It is dependent on:

AEMO’s intervention in the market with AEMO issuing FCAS targets to participants in the realm of $300/MWh for raise and lower services (due to the inability to source FCAS from outside of SA), and

Generators potentially looking to spike spot prices or increase the spot price with no doubt, gas generator running costs no doubt increasing every MWh the interconnector is out of action.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

Current weather conditions are placing an increased reliance

on the diminishing water catchments across Australia. These water catchments

store water for use by various parts of the local community including drinking

water for residents, irrigation and Electricity generation.

Stanwell recently announced water sustainability is a top

priority for its Tarong Power stations located within the South Burnett region.

Water is an essential necessity for thermal power stations to make electricity. The water is used for steam production and cooling.

Tarong power station consisting of 4 X 350MW thermal units

and a 443MW supercritical unit. These units obtain their water from two

sources, the primary source is Lake Boondooma and secondary from a pipeline

using water from Lake Wivenhoe or recycled water produced under the Western

Corridor Recycled Water Scheme.

Stanwell corporation is focusing on mitigating the impact on

the South Burnett community by reducing the usage of water from Lake Boondooma

to ensure the South Burnett community have access to drinking water. Initial

initiatives used at the power station to reduce the reliance on Lake Boondooma water

include the use of recycled water from the ash dam and stormwater.

Tarong Power Station have access to water from Lake Wivenhoe if Lake Boondooma drops below 34%, currently the Lake Boondooma’s level is 22.95% as of the (Source: SEQWater 2020). Lake Wivenhoe water also comes at an added cost. Water is currently the highest operating cost for Tarong Power Station.

An alternative to using Lake Wivenhoe water is the use of

purified recycled water from the Western Corridor Recycled Water Scheme. The

scheme is not currently in operation, however when operating and supplying

water to Tarong Power Station it will add significantly to the costs of

generation.

Tarong Power Station first used purified recycled water from

the Western Corridor Recycled Water Scheme in June 2008 following a similar

water supply limitation brought on by the 2008 drought.

As a result, the increasing marginal cost to generation

caused by the higher water cost, Tarong Power Station may change its operation

and reduce generation or dispatch its units at higher prices. Under either scenario

this may increase the cost of wholesale energy in Queensland.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The SA Government (South Australian Minister for Energy and Mining) has the power (under South Australian Legislation) to trigger a Retailer Reliability Obligation (RRO) upon informant from AEMO of a one-in-two year peak demand forecast shortfall event as published in the South Australian Gazette 17 December 2019, with the AER confirming and publishing the notice 9 January 2020. For the avoidance of doubt this means that unlike all other regions which require the Electricity Statement of Opportunity (ESOO) to predict an unserved energy event, SA can act independently without approval as such from the AER.

The RRO was trigged for South Australia on the 9 January 2020 for the following periods:

First Quarter (Q1) for Calendar Year 2022

First Quarter (Q1) for Calendar Year 2023.

The periods of concern according to AEMO’s forecasting includes:

each weekday from 10 January 2022 – 18 March 2022 for the trading periods between 3pm and 9pm EST;

**(Peak demand expected to be 3,030 MW)

each weekday from 9 January 2023 – 17 March 2023 for the trading periods between 3pm and 9pm EST

**(Peak demand expected to be 3,046 MW)

A T-3 Instrument has been created and the Market Liquidity Obligation (MLO) of the SA region’s largest generation businesses, Origin, AGL and Engie have been called upon and are to begin trading exchange-listed (ASX approved products) for Q12022 and Q12023 from 7 February 2020.

With the triggering of the RRO, the South Australian Minister has made a T-3 instrument (under NEL Part 7A 19B (1)):

Q1 2022: This T-3 Reliability Instrument applies to the South Australian region of the National Electricity Market for the trading intervals between 3pm and 9pm Eastern Standard Time each weekday during the period 10 January 2022 to 18 March 2022 inclusive. The Australian Energy Market Operator’s one-in-two year peak demand forecast for this period is 3,030 Megawatts.

Q1 2023: This T-3 Reliability Instrument applies to the South Australian region of the National Electricity Market for the trading intervals between 3pm and 9pm Eastern Standard Time each weekday during the period 9 January 2023 to 17 March 2023 inclusive. The Australian Energy Market Operator’s one-in-two year peak demand forecast for this period is 3,046 Megawatts.

With the T-3 instrument created by the SA Energy Minister, this has triggered the MLO, effectively a market making obligation on the parties identified above to reasonably offer liquid exchange-listed products for the identified shortfall periods.

Obligated MLO participants such as Origin, AGL and Engie will from 7 February 2020 begin offering exchanged-listed products for both Q12022 and Q12023.

The triggering of the RRO means retailers and large load consumers can start procuring volume for their forecast demand for Q12022 from as early as 7 February 2020, and no later than 31 December 2020, the T-1 instrument implementation date (13 months prior to the shortfall period identified).

If you would like to know more, please contact Edge on 07 3905 9220.