For the 50,342 animals that arrived at the RSPCA Queensland centre over the past year, it was a second chance at life. One of those lives belonged to 3 year old ‘Roger’, a domestic short hair ginger tabby cat. Roger had been surrendered by a family that no longer wanted him and after spending 4 months in the Wacol RSPCA shelter, was re homed. Roger was given another chance of life after being adopted by Kristy McGrath, our Head of Operations & Client Delivery, at the recent RSPCA Pop Up Adoption Day in South Brisbane. Already having two dogs and two horses, adopting Roger from the RSPCA was an easy decision when it came to adding to her animal family.

Edge has always been a big supporter of the animal community and charity foundations. And whilst choosing the right pet is fun and exciting, it takes time, planning and lots of research. To make the process easier, the RSPCA has introduced Adopt a Pet, a national website that lets you view some of the animals waiting to be adopted at RSPCA locations across Australia.

Join Edge in giving these animals another chance of life. Visit their website, and give a dog, puppy, cat or kitten a second chance to find their loving home!

By Thomas Dargue, Edge Manager of Markets & Advisory

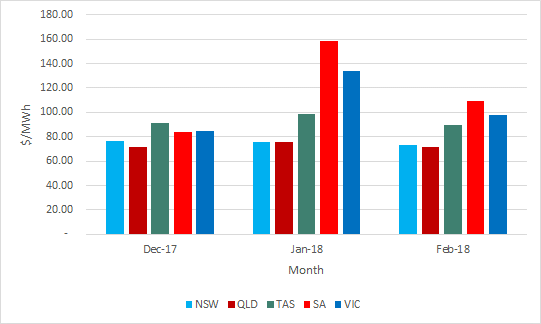

In this summer edition of the market update we look at some of the issues which is causing price differences in wholesale prices across the east coast of Australia. Since the start of summer, the divide has mainly been across the Murray river with QLD and NSW to the north and VIC, SA and TAS sitting to the South.

The summer started in December with modest spot prices across all the regions. The region with the highest price was TAS at $90.96/MWh with the lowest price being QLD at $76.56/MWh. The interconnectedness of the market means that prices in NSW was similar to QLD while SA and VIC were closer to TAS. The prices in NSW started deviating from the southern market as the interconnector with VIC became increasingly constrained. Throughout January there were large price spikes in SA and VIC increasing the average price south of the Murray. The constrained interconnector meant that the prices never travel north and both QLD and NSW had modest prices.

Figure 1 Average NEM spot prices.

Tasmania had similar prices throughout the three months however these seem to be too high for the State Liberal Government. There is an election in Tasmania 3 March 2018 and one of the policies put forward by the State Liberal Government would be a split from the NEM. TAS would still be physically connected through Basslink however would not be subject to the price setting mechanism set out for the NEM. The State Liberal Party is expecting this to result in lower wholesale prices for TAS.

Prices for summer to date has been higher in SA than any other state however there haven’t been any black outs. This is in part due to the operation of a new 100 MW battery installed by Tesla which provides energy during peak times as well as support for frequency. With an election in SA 17 March 2018 the incumbent State Labor party made its own electricity policy announcement. It would seek to further partner with Tesla to install 50,000 rooftop solar panels and batteries. When combined this would create a virtual 250 MW power station.

The Energy Security Board (ESB) realised its Draft Design Consultation Paper on the National Energy Guarantee (NEG). The NEG seek to find a balance between affordability, reliability and carbon reduction which could be politically acceptable. With the number of schemes already rejected by the Federal Government, the ESB has managed to come up with a scheme which could get bi-partisan support. At this stage there is quiet optimism however there are large concerns over the effect on contracting going forward. The ESB is looking for written submissions by 8 March 2018 and have the final design by the second half of 2018.

The forward prices generally reduced for 2019 as spot prices were less volatile than seen in previous years over summer. The exception was SA where there is still uncertainty around security of supply.

Table 1: ASX prices for Calendar Year 2019

NSW

QLD

SA

VIC

1 DEC 2017

80.75

68.11

92.94

86.55

28 FEB 2018

76.38

64.03

94.36

82.90

The forward prices were lowest in QLD where we expect a large amount of new renewable generation to be built. Concerns over sufficient supply in other regions kept prices higher.

Despite higher forward prices and the highest average spot prices in the NEM, a hydrogen electrolyser will be built in Port Lincoln, South Australia. This will produce hydrogen using excess wind and solar (i.e. when prices are low) to produce hydrogen both to power a 10 MW gas turbine but also for export purposes. By using power intermittently, it is able to ramp up during low prices and not run during high spot prices which will also stabilise the grid and allow more wind generation to be dispatched in the region (wind in SA is currently being curtailed by AEMO to avoid frequency issues). It seems counterintuitive to put an energy intensive industry in SA however for very flexible consumption of electricity who are able to take advantage of low, or even negative, spot prices there is opportunity in the state.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact Thomas on 07 3905 9226 or on 1800 EDGE ENERGY.

The ACCC released the second interim report into gas supply arrangements in December 2017. In the initial report (released September 2017) it was reported that there would be shortages in gas supply available to east coast consumers in 2018. The report found that buyers of gas were receiving offers from a reduced number of suppliers and that prices offered were above the ACCC’s benchmark prices. It was also noted in the report the lack of participation from the QLD LNG producers in the domestic market. This reported lack of participation from the LNG producers prompted the Federal Government to act. The result was the creation of a Heads of Agreement with the LNG producers which would see additional gas allocated to the domestic market. According to the second Interim Report (released in December 2017), since September 2017 the QLD LNG producers contracted 42 PJ’s of gas under long-term supply agreements to domestic buyers for supply in 2018. The majority of this gas was sold to aggregators and retailers. The ACCC’s forecast for the balance of gas was also updated in the second interim Report and resulted in an improved balance of 75 PJ’s. The change in balance has been driven by a 12 PJ increase in supply and the lower demand from the LNG producers (63 PJ). Whilst on face value the market has gone from deficit to surplus, the balance remains tight and subject to gas producers meeting forecasts.

Table 1. Gas Balance

September Expected Domestic Demand Scenario (PJ)

December Expected Domestic Demand Scenario (PJ)

Supply

1,901

1,913

Domestic demand

642

642

LNG demand

1,314

1,251

Projected Balance

-55

20

Source: ACC Gas Inquiry Report – Second Interim

According to the report, there continues to be a shortage of production in the southern states to meet demand (SA, NSW, ACT, VIC and TAS). As a result, these states will continue to rely on gas transported from QLD. Additional costs to transport gas from QLD to VIC and SA are currently between $2/GJ and $4/GJ. Transporting gas south from QLD is not only expensive but due to limited firm capacity in key pipelines is not always feasible. Firm capacity in these key pipelines is predominately booked by the major retailers. It was examined by the ACCC if the major retailers were making spare capacity available to other users on major pipelines through secondary trading. It was found that on the major pipelines this was not the case however, there was some evidence to suggest this may have been occurring on the less critical pipelines. Since the ACCC investigation it has been observed that the retailers have increased the availability of spare capacity to other pipelines participants improving competition.

FIRM CAPACITY – The amount of transmission guaranteed to be available to the shipper – up to MDQ & MHQ every day

AS AVAILABLE CAPACITY – This capacity is typically spare contracted capacity that is offered on the secondary market. As can be disrupted or delayed, it is not necessarily guaranteed.

The ACCC expects that transportation costs will start to come down as regulatory reforms begin to take effect.

Domestic prices to large C&I customers were around $16/GJ in early 2017 and even higher for smaller business customers. Since July 2017, it was reported that prices between $8/GJ and $12/GJ were achieved by large C&I customers.

GAS PRICES

Across each of the east coast trading hubs January average prices were higher than the Q417 average.

Table 2. Hub Prices

Adelaide price ($/GJ)

Brisbane price ($/GJ)

Sydney price ($/GJ)

Melbourne price ($/GJ)

Q417

$7.14

$7.68

$7.12

$6.20

JAN18

$ 8.10

$8.16

$9.71

$8.64

FEB18

$9.29

$7.33

$9.71

$8.67

Source: AEMO

Recent news

Four projects have received funding from the South Australian Plan for Accelerating Exploration (PACE) gas program’s second round. The program was designed as part of a suite of measures to increase investment in local gas production and to ease price pressure in South Australia. The four projects to receive funding were:

$6.89 million for the Santos-Beach Cooper Basin project to deploy a heat-energy recovery system to offset natural gas used to run the Moomba petroleum processing plant

$5.26 million for the Senex Cooper Basin Gemba exploration/appraisal project

$6.89 million for Beach /Cooper Energy’s Dombey project in the Otway Basin

$4.95 million to the Rawson/Vintage Nangwarry project in the Otway Basin

Under the program, gas extracted through the PACE program must first be offered to local electricity generators, enhancing the affordability of supply. Whether the cheaper gas is passed onto end customers by the gas generators is more difficult to say.

Moving north to QLD, Senex’s 100% owned Western Surat Gas Project recently recorded a significant milestone, which was an all-in well cost of $1.2 million. The strong results have promoted Senex’s reputation in the market and has encouraged Project Atlas, which is another Surat Basin project expected to bring first gas in 2019, to be sold to the domestic market.

On 12 December Independent Scientific Inquiry into Hydraulic of Onshore Unconventional Reservoirs in the Northern Territory releases its draft final report. The overall conclusion of the report was:

“The overall conclusion of the Report is that risk is inherent in all development and that an onshore shale gas industry is no exception. However, if the recommendations made in this draft Report are adopted and implemented in full, those risks may be mitigated or reduced – and in many cases eliminated altogether – to acceptable levels having regard to the totality of the evidence.”

Since the release of the draft final report the panel has engaged with the Northern Territory community, Government, Industry, environmental groups, and other relevant stakeholders about the content of the report. This is the last opportunity for the Territorians to express their views on the inquiry.

The final round of regional consultations concluded mid-February and the final day for submissions due to the panel is 25 February 2018. At this stage the panel has committed to providing the Final Report to the government in March 2018.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220 or contact your Edge Portfolio Manager.

We are seeing a significant increase in large users exploring renewable generation off-take opportunities. This includes behind the meter build-own-operate or power purchase agreements (PPAs), and offsite commercial arrangements otherwise referred to as corporate PPAs, synthetic PPAs, or simply contracts for difference (CFDs). The reasons are mixed. Some are looking to meet future corporate emissions targets. Others are aiming to achieve lower energy costs. Some are looking to further diversify procurement strategies. All are fearful of missing out on the next big opportunity.

Edge are actively involved in taking large electricity users through the process of assessing, and where feasible, entering into arrangements with renewable generation. We provide a range of services covering everything from practical energy market expertise and advice through to strategy development and implementation and even transaction support. This is particularly helpful where the renewable generation forms part of a new or existing electricity sales agreement as negotiating terms can otherwise be difficult. Large mining, transport, agricultural and manufacturing clients are amongst those leading the way. Elsewhere in the market, we have all seen the announcements from users such as Sunmetals, Telstra, Onesteel, Sunshine Coast Council, Universities and smaller aggregated buying groups (to name a few). The list is growing rapidly.

Looking beyond the consulting jargon, the diverging spectrum of price forecasting curves, and the race for the next Renew Economy or AFR headline, are these deals really the right thing for your business? Absolutely, they can be. But they may also not be. It is critical that you understand the current electricity market including renewable generation, and the potential financial benefits and costs these opportunities can bring to your business. Edge can work with you to identify and understand these critical components to ensure you take the right direction when considering renewable generation in your portfolio. It is important to consider how adding renewable generation will affect your current position including your electricity contract.

You’re shown the aggregate market price of electricity and LGCs today and a comparable renewable generation blended off-take price. Depending on the region and generation project, you’re looking at $130 to $150/MWh on the market against $60 to $70/MWh for renewable generation. The savings appear staggering. But some things may be too good to be true and the devil certainly is in the detail.

Term

These opportunities are long term propositions, typically seven to twelve years though can be as long as twenty years or as short as three years. A lot can happen in this time and only one thing is for certain, things will change. Supply and demand profiles will change. Project and market pricing will change. Governments and their priorities and policies will change. Depending on your corporation’s view on being quarantined (for better or worse) from these changes, you may lean towards all longer term, a blend of longer and shorter term, or no longer term contracting.

Project Risk

Renewable project developers are everywhere. Long haul business class cabins are filled with them. Virtual office spaces have never had it so good. But not all have the experience in developing projects in Australia, therefore lacking experience with NEM based network service providers (NSPs), Australian government and council bodies, EPC contractors, and the like. Go to any NSP public forum and you’ll see first-hand the challenges that face NSPs around renewable project connections. Be it sheer volumes of enquiries, network or timing constraints, project risk is rife. An off-take start date can quite literally make the difference between a business case supporting the opportunity or not. Partnering with a credible counterparty and / or managing project risk is critical.

Price Forecasting

The harsh reality is, we spent 2017 being privy to too much price forecasting that existed simply to suit the narrative. You can make generation opportunity in or out of the money with a suitable forecast curve. Price forecasting plays a significant role in assessing the optimal renewable generation project and the potential value and risk that sits within in it. Projecting future spot prices is a quantitative minefield. There are a few well known modelling tools utilised by equally well-known consultants to generate spot price forecasts in the NEM. Edge also generates in house spot price forecasting. Whomever you utilise to produce future price curves, challenge the inputs and demand shape on the outputs. With significant volumes of renewable generation set to enter the NEM and aging fossil fuel plant preparing to exit, we are moving into a new dynamic in the NEM. The characteristics of the supply curve are changing considerably. As storage technology advances, the behaviour of intermittent generation too will advance. As users are forced to explore demand side management (DSM) opportunities, the demand profile will also change. Five-minute trading intervals will change supply and demand behaviour. To adequately assess any renewable generation or off-take opportunity it’s about the expected spot outcome and the sensitivity around this result, measured in each trading interval. Having a high and low case based around randomly selected forced outages doesn’t even begin to address the uncertainty in the electricity market. Even if a project is priced firm to a flat mega-watt (MW) profile, understanding the potential impact to the shape the merits of the firm pricing against other procurement strategies.

Regulatory Risk

Either we are getting older and more in tune with the volatile nature of politics, or politics has taken regulatory racket ball to the whole next level. Investment in new generation in the NEM has previously stalled due to policy uncertainty. The more recent run of high electricity prices is testament to this. Just when the market does what markets are supposed to do and responds to price drivers with new entrants and technological advancements, our policy makers inject more uncertainty in the form of a National Energy Guarantee (NEG). The end game of the NEG is noble. To promote that we meet our international emissions commitments, whilst ensuring our electricity is reliable, secure, and of course affordable. Achieving this whilst not forcing any politician to back down from previously stated principals. The practical application of the proposed design however is a very long way from readiness, and in its current form is alarmingly at risk of causing segregation and market power that can only result in higher energy prices. Meanwhile the Government has cast a dark cloud over the application of the Renewable Energy Act, and specifically the ability for renewable energy projects to receive certificates if they are commissioned after the target date of 2020. It’s a risk that not even all the developers are aware of. As an off-taker you must make it your priority to be across it and manage it.

Shape Risk and Firming

Renewable generation is intermittent. The question remains; what happens when the sun isn’t shining, or the wind isn’t blowing? Storage solutions are on the rise, but the dispatch limitations and costs still make it very challenging to get the business case across the line. Clients who are looking to integrate renewable generation in their portfolio must be aware of the risks associated with shape risk. This includes managing their shape with the overall shape of their hedge portfolio (tenure, type, etc.) and spot risk. How can one best introduce intermittent generation (or intermittent offtake) into a portfolio, and what is the most efficient and effective means to manage this risk. Firming products are one of the most sought-after products in the NEM today. Physical solutions have their role in mitigating some shape risk and include DSM, onsite generation, and storage solutions. Financial solutions also stand to play a significant role, including both traditional electricity derivatives and weather derivatives. Securing firming products is undeniably challenging. Hydro and gas generators have five-minute settlement to consider. Furthermore, gas generators need to clear long-term fuel supply hurdles. Coal generators may not be so eager to firm a product that will ultimately stand as the perfect competitor to their own offtake. Edge work closely with clients to understand shape risk and firming solutions. We actively engage with the wholesale market to seek and deliver solutions that work best for each individual client.

Settlement

Settlement of third party PPAs need not be complicated. In fact, it need not be independent of your electricity invoices. Edge has negotiated PPAs that settle directly between the project and off-taker. We have also negotiated settlement services with retailers to ensure consumers benefit from longer term renewable generation whilst still only receiving monthly invoices form their retailers. Understanding the cash flow implications and adequately addressing credit counterparty risk is all critical but certainly manageable.

Accounting

There are accounting implications as to how these arrangements are structured. Whilst we are across these due to our involvement in large offtake deals, we are not an accounting firm. We would strongly recommend that any consumer exploring these opportunities ensures their accounting advisors are across implications such as implied lease agreements, impacts to the balance sheet, and / or derivative accounting.

Whatever stage your organisation is at in considering Renewable Energy as a part of your electricity portfolio, Edge can help. If you would like to learn more about Edge, please visit edge2020.com.au or alternatively you can call one of our team directly on 07 3905 9220 or on 1800 EDGE ENERGY.

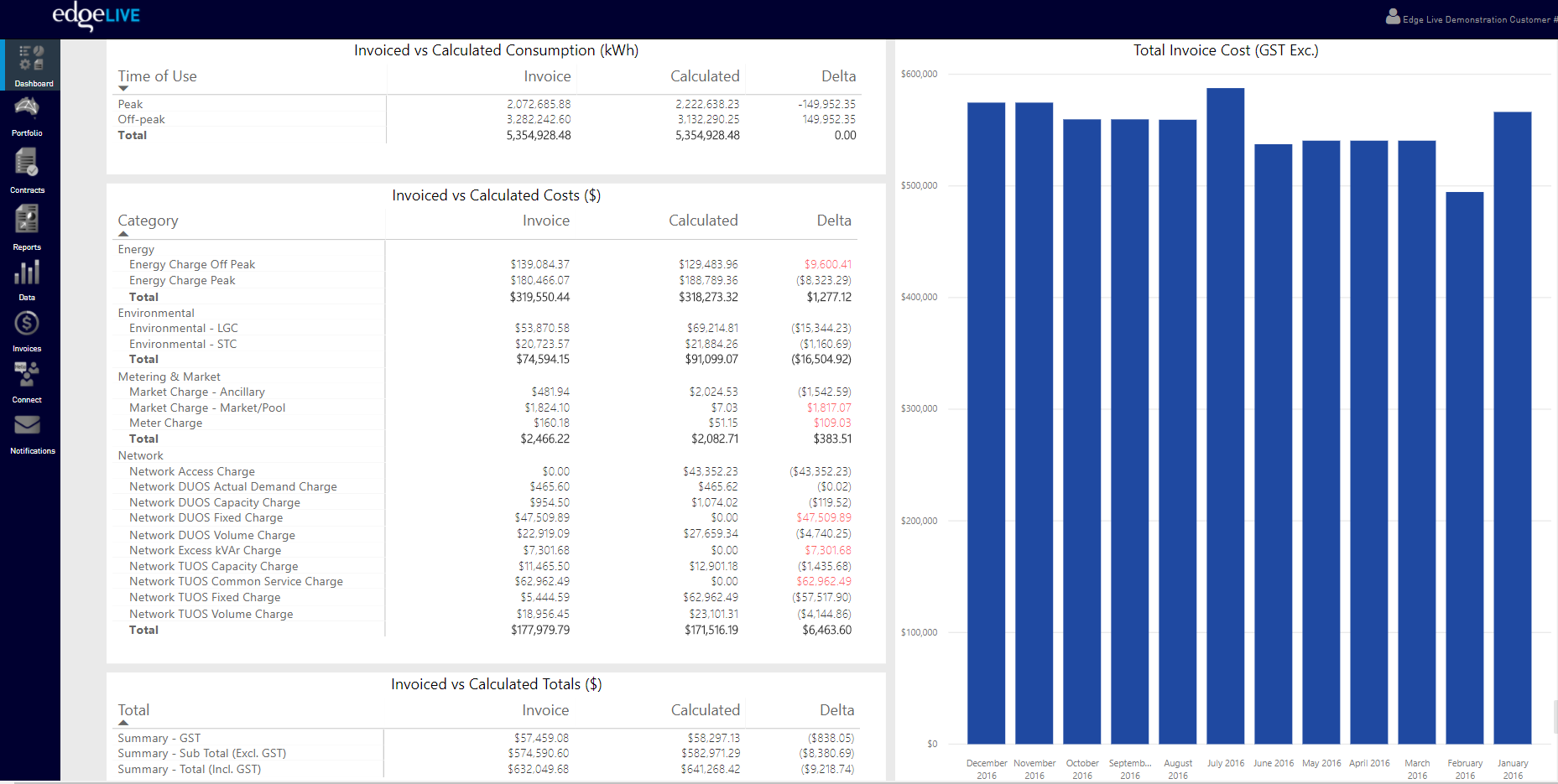

In addition to Snapshot functionality which provides you with information relating to your current and forecast spend and consumption, you can now access your Invoice Reconciliation and Accrual outcomes instantly within Edge Live.

Your Edge Portfolio Manager undertakes your Invoice Reconciliation services the same business day that your final invoice is issued by your Retailer. From here, the payment advice and outcomes are published instantly on Edge Live. You will receive an email notification that the reconciliation outcome is available, with links through to the Invoice Reconciliation Report. Providing you with details of the invoice outcome, broken down to the detailed levels of energy, network, markets and other costs.

Figure 1 Invoice reconciliation outcome in detail.

Viewing the results is easier and more efficient than ever before. View them in Edge Live directly from your web browser rather than having to open excel and find the information relevant to you. Though if you need to, the data can be exported to excel easily with the click of a button within Edge Live.

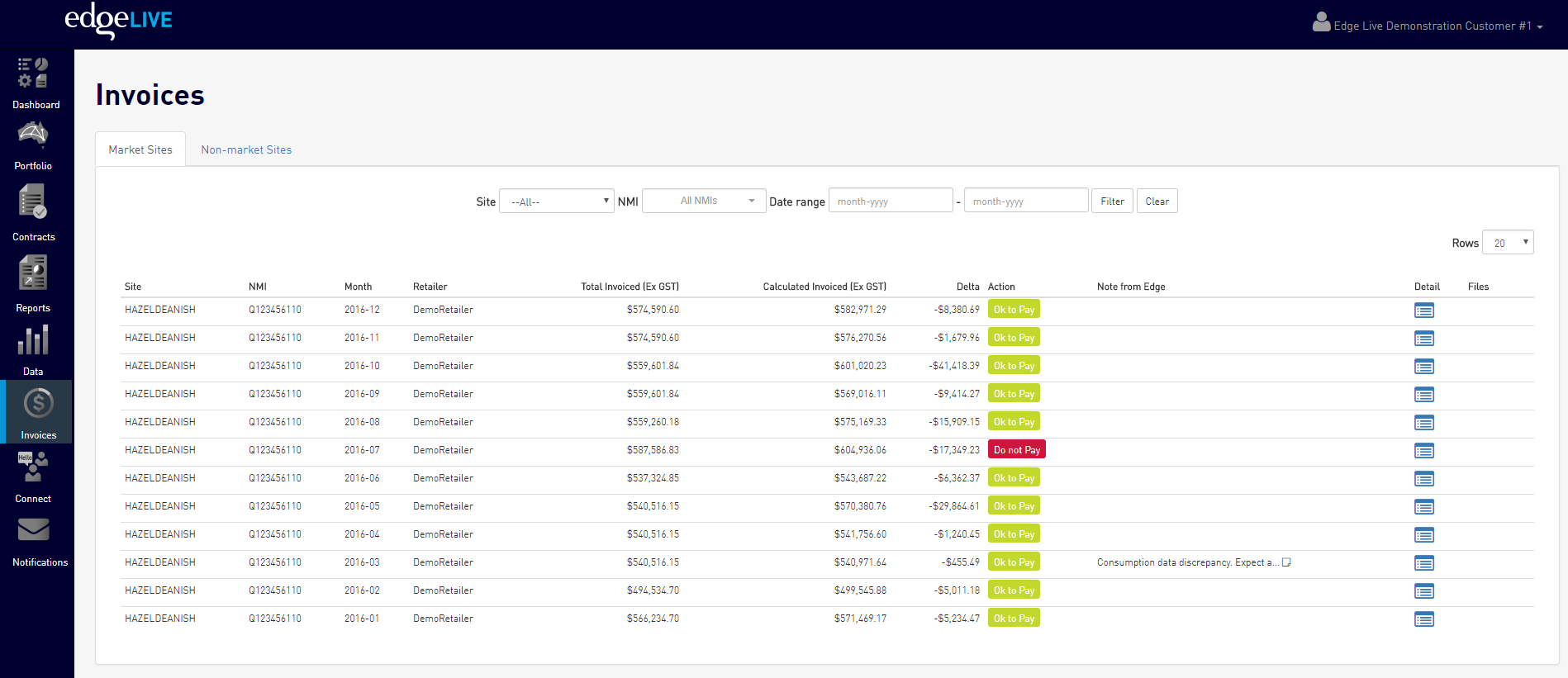

You will be provided with the invoice reconciliation outcomes, advice on whether to pay or not to pay and any additional personalised comments from your Portfolio Manager relating to your portfolio and individual sites.

Figure 2 Invoice reconciliation notification at an invoice level.

Your monthly Accruals reporting is also available via the online portal. Again, providing an easy and efficient way to advise your finance teams what the expected electricity spend of your portfolio will be as you near the end of each month.

And don’t forget about the existing Dashboard module. Filter by site and drill-down on specific time-frames of your electricity portfolio so that you can get a clearer view of consumption and costs.

Your Portfolio Manager will be in touch soon to discuss these new features with you, and ensure you have access to Edge Live as well as answer any questions you may have.

We have some exciting features planned for the remainder of 2018. If you have any feedback or suggestions on how Edge Live can be of more value to your business please do not hesitate to let us know, and we will do our best to incorporate this into our Edge Live development roadmap.

To learn more about Edge Live functionality click here, or speak with your Edge Portfolio Manager.

The Children’s Hospital Foundation helps sick kids today and tomorrow by funding life-saving medical research, investing in vital new equipment, and providing comfort, entertainment, support and care for children and their families.

To support this great charity, Edge will be attending The Coffee Club Telethon Ball for the 2nd year running on the 18th of this month.

Unfortunately this event sold out quickly, however there’s a lot you can do to support a child with an injury, serious illness or life threatening disease. You can donate money to help save precious young lives. Donate your time to make a difference at our children’s hospital. Or raise funds for vital research and equipment, spread smiles and support families through difficult times.

You can make a difference to sick kids and their families today and tomorrow. To find out more visit the Children’s Hospital Foundation site at www.childrens.org.au and be sure to tune into Channel 9, Saturday 19 November for the annual Telethon.

We’re all about providing a tailored and specialised service to our clients. But we also know you often need quick access to information regarding your energy consumption and spend. This is why we’ve developed Edge Live.

Edge Live is a secure, online information portal that gives you instant access to contracts, portfolio information, reports, data and so much more. The portal provides you with instant access to the information you need to make informed choices for your business.

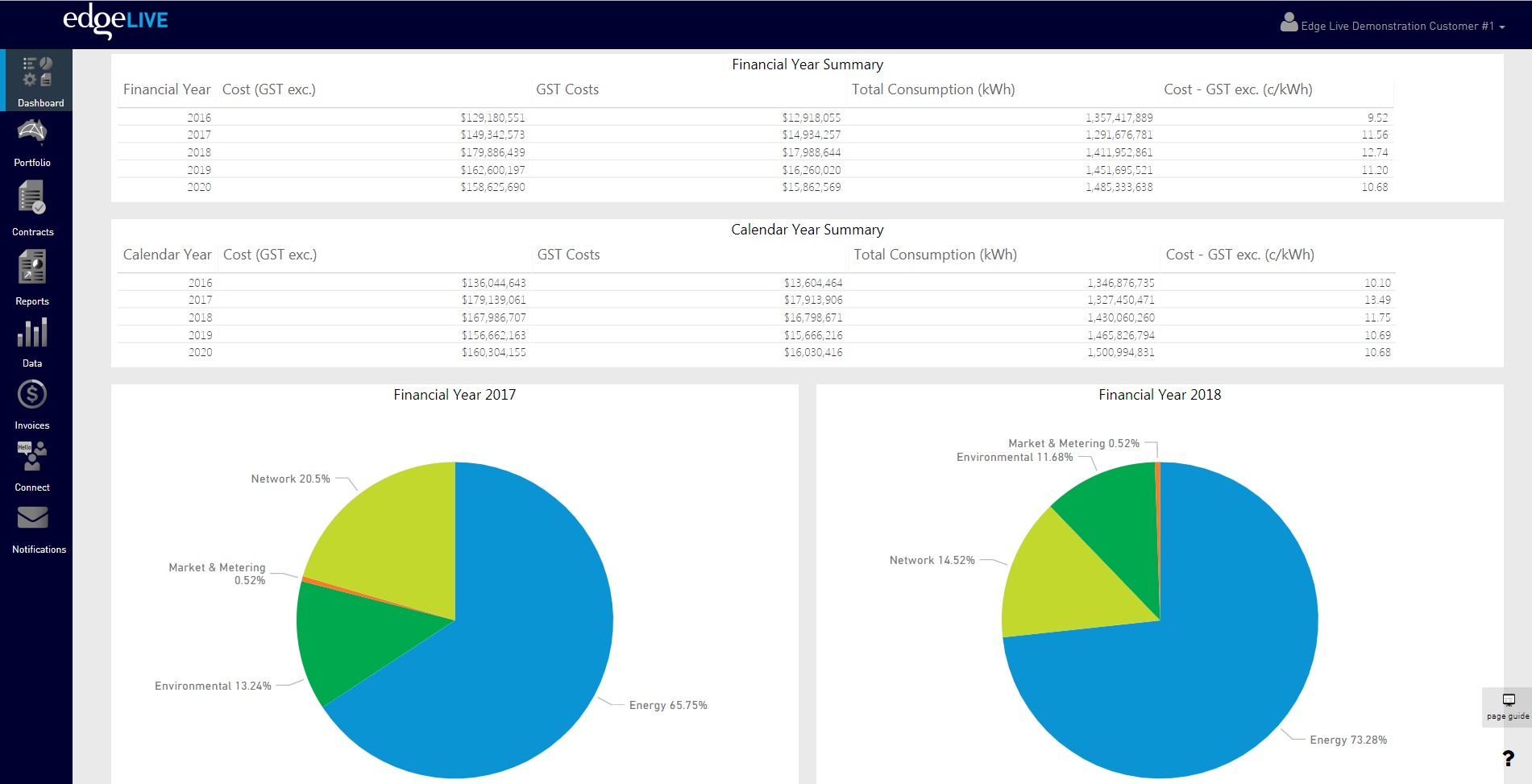

Our latest enhancements to the Edge Live software is our interactive Dashboard module.

Interactive Dashboards

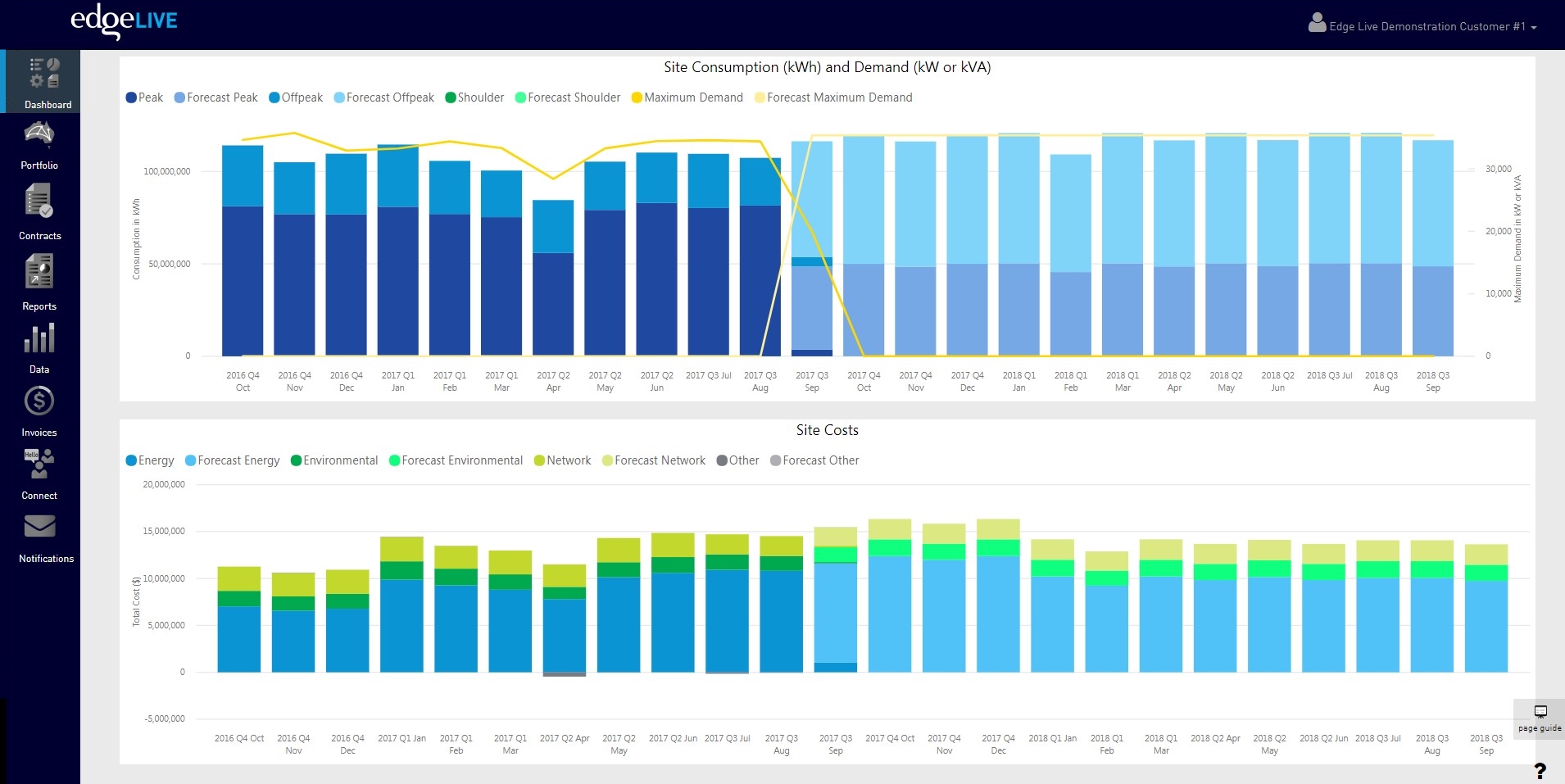

Edge Dashboard provides you with an interactive graphical portal that allows you to view your consumption and energy costs across a chosen period. The functionality of the dashboard allows you to filter data to a specific financial or calendar year, whilst also providing you with the ability to set your own date range.

Figure 1 Cost data being displayed by financial and calendar year both in table and graphical format.

It also provides you with the ability to drill down to specific sites and/or regions, depending on the portfolio or type of reporting that you wish to obtain information for.

Figure 2 Graph illustrating site consumption and demand across a period of months and a graph illustrating site costs across a period of months.

If you require more information than the standard dashboard provides, bespoke dashboards can be prepared for you in conjunction with our in-house IT Team and your dedicated Portfolio Manager.

Other Interactive Modules

Edge live has many modules that will provide you with valuable data and information that is critical to managing your energy portfolio. These modules include:

Counterparty contracts;

Portfolio information;

Reports, and

Data.

To read more about Edge Live functionality click here, and call your Portfolio Manager on 07 3905 9220 to book in a demonstration.

The electricity market is in a state of confusion as a result of poor Federal and State Government policy. The Market Operator, AEMO, released the Electricity Statement of Opportunities during September. The Statement warned of supply shortfalls during the first three months of 2018 and a heightened risk of unserved energy over the next 10 years.

On 17 October the Federal Government announced the National Energy Guarantee (NEG). The Guarantee is the model that will see energy being delivered to consumers reliably and affordably whilst also meeting our international emission commitments. The NEG is an alternative to the Clean Energy Target introduced by Dr Alan Finkel in his Finkel Review. Since the announcement of the NEG, there has been minimal feedback by the Federal Opposition and some of the State Governments. These governments have made it clear they are waiting on further detail before giving their support. Without support from these governments it will be difficult for the NEG to get off the ground. Edge are awaiting further announcements and modelling from the Federal Government as there is insufficient detail to form a view on the impacts or functionality of the Guarantee for producers and consumers of energy.

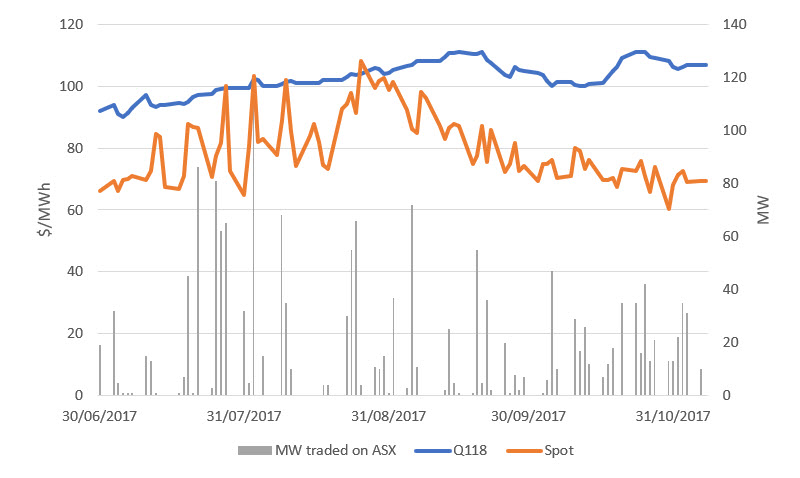

The combination of forecast shortfalls in energy supply, and a national energy policy that lacks detail, has resulted in the price of forward contracts creeping up despite softening spot prices. This has been particularly evident in NSW.

Figure 1 NSW daily average spot price verse CAL18 price and volume traded on the ASX.

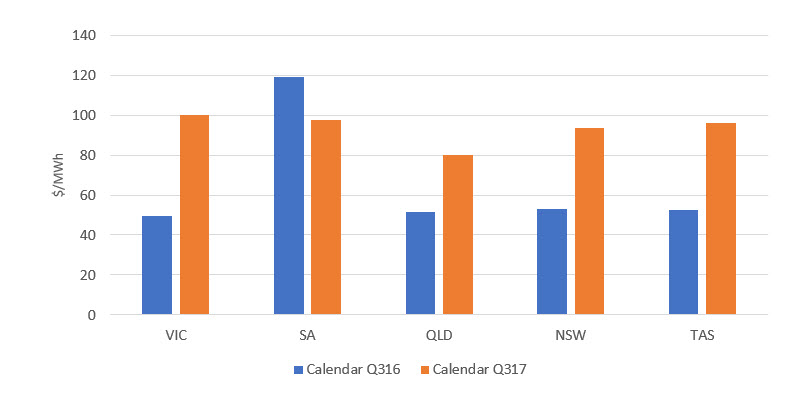

With the exception of SA, average spot prices for Q317 are significantly higher than Q316 prices. This represents a fundamental shift in the market.

VIC

SA

QLD

NSW

TAS

Calendar Q317

100.01

97.74

79.93

93.57

95.84

Table 1 Q317 average spot prices as at 7 November 2017.

Figure 2 Q316 verse Q317 average spot prices.

With valid concern around shortages in supply, medium to large energy consumers are looking for alternatives to reduce costs and/or hedge price risks. A credible alternative is a Power Purchase Agreement (PPA); entered into directly with a generator. PPAs can be facilitated with any kind of generator that is willing to offer one. Typically, these are renewable energy projects offering 10 – 20 year agreements at defined prices. This type of offtake agreement is generally required prior to a new renewable project receiving financing. Offtake agreements from renewable projects do not suit all customers and the following points are some key considerations that should be taken into account before entering a PPA with a renewable generator:

Ability to commit to a volume and price for 10 or more years

Correlation of your demand and the output profile of the renewable generator

Business view on hedging commodities

Click here if you would like to read more about how Edge is assisting customers to reduce costs through the implementation of PPA’s.

Supply Near Term outlook

Spot prices are expected to be volatile and high due to a shortage in supply. Particularly in the first three calendar months of 2018 in SA and VIC. This expectation is a driver behind the Reliability and Emergency Reserve Trader (RERT) and a reason for forward contracts being traded at high prices.

VIC

SA

QLD

NSW

Q118

146.00

159.00

105.35

106.76

Table 2 Q118 Forward Contract Prices as at 7 November 2017.

The second round of the Long Notice RERT was released on 6 September 2017. The purpose of the RERT is to provide AEMO with the capability to maintain power system reliability and system security by utilising reserve contracts. In order to become a member of the RERT Panel, panellists need to either provide generation or load reduction.

Submissions were due on 20 September and contracts are required to be executed by the 31 October 2017. Currently, there is a Medium to Short Term RERT open to tender which is scheduled to close on 17 November. Participants are asked in this tender what their reserve availability will be in the period 1 November 2017 to 31 March 2018.

The recent commitment from LNG producers to make more gas available to the domestic market should alleviate some of the predicted high electricity prices. It has to be noted however, that this additional gas is in QLD which is a long way from SA and VIC where the main concerns sit. This gas is more likely to relieve prices in QLD which in turn should help to mitigate high spot prices in NSW, though impacts will be marginal further south.

The Australian Energy Market Operator (AEMO) released its updated Gas Statement of Opportunities during September. The report indicates that in eastern and south-eastern Australia, there is potential for an annual energy shortfall in the domestic gas market of 54 petajoules (PJ) in 2018 and 48 PJ in 2018. AEMO warned that the shortfall could be higher in a variety of plausible circumstances that could increase demand for gas by household and business consumers, and for gas-powered generation of electricity (GPG) in the National Electricity Market (NEM). AEMO’s estimates that the shortfall could be as high as 107 PJ in 2018 and 102 PJ in 2019. This forecast was quickly followed by the Federal Government requesting major LNG producers to bridge the supply gap or face the implementation of the Australian Domestic Gas Security Mechanism (ADGSM). The LNG producers agreed to the Prime Minister’s request to make gas available. Had they not, the Federal Government has the power to implement the ADGSM which is a mechanism designed to restrict gas exports to increase domestic supply.

The Sole Gas Project is a new source of gas for the south east. The project is estimated to bring an additional 25 PJs of supply to the market each year, of which some is already contracted. This is the first offshore project in VIC to be sanctioned in almost a decade.

Still on the topic of increasing supply of gas to the east coast, the Northern Gas Pipeline is being promoted by owners Jemena, as being operational from the end of 2018. This is despite delays caused by negotiations with traditional owners of land and issues with the construction partner. Once the pipeline is complete it will have capacity to transport 90 TJs per day from Tennant Creek to Mt Isa. The challenge will be delivering gas to the east coast at a competitive price and achieving a level of increased supply that is sufficient to impact prices.

Following the NT Governments announcement of a moratorium on hydraulic fracturing of onshore unconventional reservoirs and the initiation of an Independent Scientific inquiry into Hydraulic Fracturing of onshore unconventional reservoirs, an interim report was released during July. The report provided some high-level conclusions regarding the environmental, social, cultural and economic risks associated with hydraulic fracturing for shale gas in the NT. The final report is due March 2018 and will be critical in guiding the NT government on whether to lift the moratorium. During September the Federal Government pressured the NT government into lifting the moratorium in the interest of making more gas available for domestic consumption.

Difference between Conventional and Unconventional gas…

Unconventional gas rests in relatively impermeable rock. The low porosity of the rocks is why, as opposed to conventional gas, ‘artificial stimulation’ is required. Artificial stimulation is where fracturing or “fracking” is required to disrupt the rock and release the gas. Unconventional gas includes Coal Seam Gas (CSG), shale gas and tight gas.

Conventional gas has moved from its original source rocks and is now resting in more permeable rocks and has then been trapped under a seal of impermeable rocks. Collection of conventional gas is easier as the gas accumulates in confined spaces and therefore allows for strategically placed wells to take advantage of areas of accumulated gas.

Gas Prices

Wholesale gas prices were lower for Adelaide and Brisbane and higher for Sydney and Melbourne relative to the same period last year. Unlike last year there were no significant price spikes in Adelaide or Melbourne.

Adelaide price ($/GJ)

Brisbane price ($/GJ)

Sydney price ($/GJ)

Melbourne price ($/GJ)

Q316

$9.27

$7.13

$7.53

$8.48

Q317

$ 8.11

$6.71

$8.94

$8.72

During September there was an increase in average temperatures which lowered demand for domestic heating gas and consequently there was some softening of wholesale prices late in the month.

C&I customers are generally facing increased prices as they come off old contracts. Prices quoted by gas suppliers have a relatively wide range and are subject to swings in consumption and tenure of agreement. The higher contract prices have prompted consumers to ask questions about alternative supply options and there has been an increase in interest into participation in capital city trading hubs.

Gas supply is a key feature of the recently announced National Energy Guarantee (NEG). Gas plays a key role in any emissions reduction policy due to its relatively low emissions and responsive nature of gas fired power stations. Within the NEG there is $90 million allocated to securing medium term supply. The funds will go towards the following initiatives:

Geological and Bioregional Assessments program to examine new gas reserves and support increased domestic supply by assessing the environmental safety of unconventional gas;

Development of new onshore gas in the NT and east coast;

Accelerate the work of the Gas Market Reform group to improve access and transparency;

Assessment of benefits in construction of new gas pipelines in the north and west of Australia to the south east via Moomba in SA; and

Examination of constraints on increasing gas supply on the east coast such as regulatory barriers and inconsistent policy.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3232 1115 or contact your Edge Portfolio Manager.

How does your business procure its electricity? More importantly how does your business manage electricity price risk?

Do you secure a long-term agreement only to file it away not to be seen for several years? If this is the case, then it’s time for a check-up because you may be placing your business at risk.

If your business is situated on the east coast of Australia it’s connected to the National Electricity Market (NEM). This market operates every second of the day, 7 days per week, 365 days per year. It’s the platform that connects electricity producers and consumers. The NEM enables electricity to be treated as a commodity and consumers can enter into forward contracts to manage their commodity risk in the same way other commodities are managed.

If you haven’t reviewed your electricity risk guidelines in recent years, it is likely you contracted with a retailer for a 2-3 year period. By entering into a long-term rate agreement you are foregoing opportunities to secure potentially lower electricity prices if there is a decline in prices.

In the current energy market it’s important to take a proactive approach to securing your electricity rates. This can help mitigate the risks of price increases and capitalise on price decreases. This approach enables consumers to secure electricity rates on a quarterly and region basis and is often referred to as progressive purchasing.

The volume of electricity that your business uses is a significant consideration when determining your appropriate risk tolerances. The more electricity your business uses, the greater the financial risk.

If you are unsure about how to approach your electricity procurement or are interested in understanding more about risks associated with electricity purchasing, please contact us on 07 3232 1115 to speak with one of our Portfolio Managers.