The CEO Business Prospects Survey conducted by The Australian Industry Group (AI Group) has identified a concern among CEOs about a rise in energy prices in 2017.

The annual survey received responses from 285 CEOs representing all major non-primary private-sector industries Australia-wide. The industries were grouped into mining services, manufacturing, construction, and services. Edge was particularly interested in the results as our core business is supporting clients from these industries in managing their energy costs and portfolios.

Many respondents are cautiously optimistic about business conditions in 2017 but maintain an almost neutral position when it comes to business investment and employment. There are several positive factors that contribute to this optimism including; low interest rates, low inflation, low unemployment, and a lower trading range for the Australian dollar.

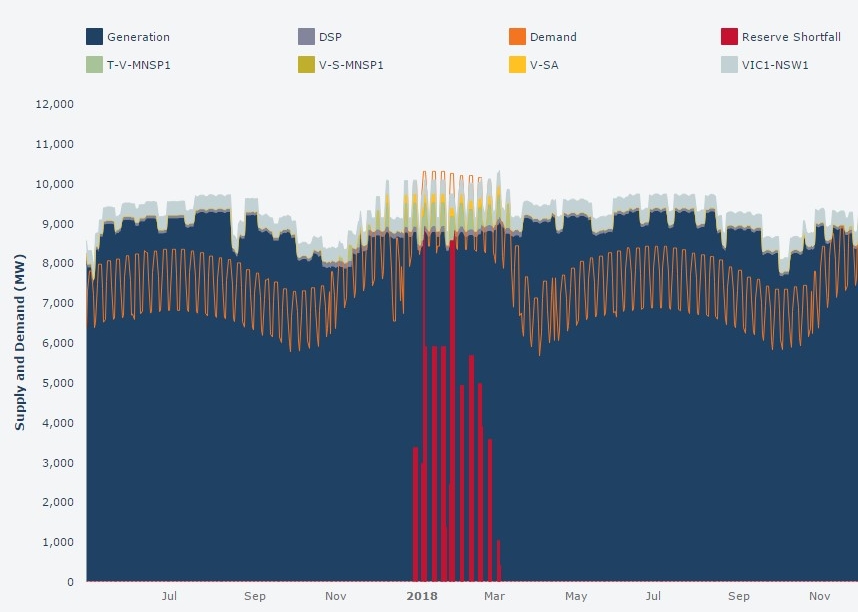

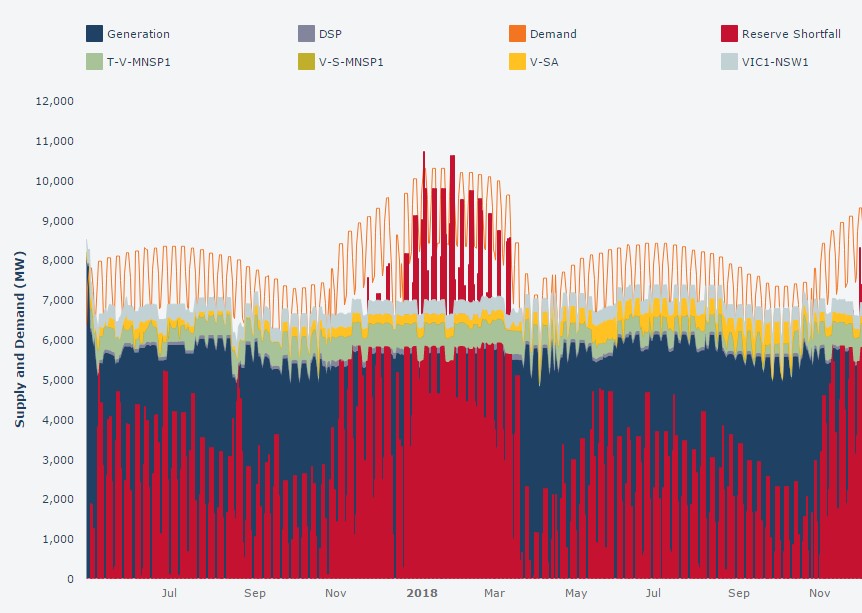

Data from the survey identified several key areas CEOs were concerned about for 2017. One of these was the expectation that energy prices would negatively impact their business throughout the year. 51 per cent of CEOs expect their energy costs to rise in 2017. This is in addition to some reporting a doubling or tripling of their energy costs in 2016. These are real concerns, and ones we have seen first-hand.

It was interesting to note that businesses involved in this survey were more in favour of increasing sales or developing new products rather than managing operational costs. Although sales and product development are important, prudent management of operational costs should be an ongoing priority for businesses. Especially the costs that can be structured in a way to reduce risk and exposure to changeable markets.

Edge understands the effect energy prices can have on a business. With the benefit of extensive experience and daily immersion in the market, we have a depth of knowledge in the energy industry that can’t be matched. It has enabled us to develop procurement strategies and reporting that are focused on mitigating risk and reducing energy costs. Our clients get the benefit of years of experience when they work with us. Working closely with our clients and tailoring solutions for their energy portfolios has resulted in savings of millions of dollars for them over the last decade.

Read the full report at http://cdn.aigroup.com.au/Reports/2017/Business_prospects_Jan2017.pdf

How are energy prices affecting your business in 2017? Contact us to see how we can help.