QLD energy retailers have been requested by the QLD Premier to pass on lower electricity prices to customers or face public shaming and increased competition through a new government owned retailer.

The lower electricity prices are driven by the QLD Governments intervention in the market which consists of ordering Stanwell Corporation (state owned) to lower wholesale prices, the $770 million subsidy for non-solar households for QLD Solar Bonus Scheme and the recommissioning of the Swanbank E Gas power station. Premier Palaszczuk promised to name and shame retailers who did not commit to the pledge by this Friday. Moving forward, Ms Palaszczuk confirmed that her government and the QLD Competition Authority would be monitoring retailers on a quarterly basis. If it is found that retailers are not passing on the savings then she would order a re-entry by the government into the retailing sector.

The Federal Government has released its Powering Forward Plan which seeks to reduce electricity prices while still delivering reliable energy and meeting Australia’s international commitments on carbon reduction. The plan is wide ranging and includes direct subsidies to vulnerable households as well as improved transparency in the gas market.

The Plan will look at putting obligations on the retailers to secure a minimum amount of synchronous generation. It was also confirmed that the Government would not be implementing the Clean Energy Target proposed by Finkel, however will obligate retailers to purchase an amount of low-emissions generation. The targets have not been set at this stage.

It was also reported that renewable generators which were built after 2020 would not be eligible to receive large-scale generation certificates. Any renewable generation built before 2020 would still be eligible (subject to current eligibility criteria) to create certificates out to 2030.

The market responded with increased prices. Until there is further clarity, the market will remain nervous.

If you would like to know more about this announcement and how your business may be affected, please call one of our team members on 07 3232 1115 or contact your Edge Portfolio Manager.

The large electricity retailers have followed up on their previous meeting earlier this month in Canberra, meeting with Prime Minister Malcolm Turnbull in Sydney today. The topic of discussion was in regard to retailers contacting their existing customers who are on high standing electricity rates and informing them of more competitive deals available to them. The retailers agreed to the PM’s request to make contact with their customers on high standard rates and will be writing to over 2 million customers. This is one of the measures taken by the Turnbull government to reduce energy costs for Australian households.

It was noted that the energy retailers stressed to Mr Turnbull the need for energy policy certainty. This relates to whether or not the Turnbull Government will accept the final recommendation from the Finkel Review to implement a Clean Energy Target. On Monday night, Mr Turnbull appeared on the ABC’s 730 Report. When asked if his government would make a decision on the Clean Energy Target before the end of year, Prime Minister Turnbull could not commit but insisted that his government was taking a detailed considered approach to the matter.

Earlier today the Victorian Premier Daniel Andrews and the Minister for Energy, Environment and Climate Change Lily D’Ambrosio announced the introduction of legislation for Victorian Renewable Energy Targets (VRET); the largest renewable energy auction in Australia. The ministers also announced the award of contracts for two large scale solar plants to supply energy to Melbourne’s tram network.

Daniel Andrews announced that the Victorian Government would conduct a reverse auction for 650 MW of renewable capacity. Details of when the auction would be taking place were not provided. This move by the Victorian Premier will help towards achieving the states renewable energy target of 25% by 2020 and 40% by 2025.

Earlier this week the Palaszczuk Government launched the Renewables 400 program; a reverse auction for 400 MW capacity. The program invites parties to participate in a reverse auction for wind, solar and storage capacity. As part of the project up to 100 MW will be allocated specifically to storage capacity. An Expression Of Interest (EOI) will commence in late August 2017. The aim of the project is to:

• Diversify the sources of Queensland’s electricity generation

• Support system security and reliability

• Accelerate the deployment of energy storage in Queensland

• Support local business and employment

As was the case in Victoria, this project will move Queensland closer towards achieving its target of 50% renewable energy by 2030.

The Queensland Government has announced CS Energy; which is wholly owned by the Queensland State Government, will form a 50/50 partnership with the privately owned Alinta Energy. The newly formed company would provide discounted electricity prices to residential customers and small businesses in South East Queensland.

The new company would offer a 2-year electricity contract with a headline 25% discount of usage charges. This offer is currently marketed on Alinta’s website as a Home SaverPlus.

The Queensland Government is urging other retailers to offer similar discounts and has encouraged them to approach the government owned corporations to strike similar deals and pass on savings. There are currently no plans to extend this offer outside South East Queensland.

Electricity retailers will increase their standard pricing from 1 July 2017 for all states in the National Electricity Market (NEM), with South Australia (SA) tipped to have the largest increase.

As part of their annual review of energy tariffs, the three biggest retailers have cited increased wholesale energy costs as the main reason for the significant increases. The retailers say the increased wholesale costs have been caused by the closure of baseload coal-fired generation and the increased costs of gas.

Residential customers in SA will see an average increase of 19.9 per cent from EnergyAustralia, 18 per cent from AGL, and 16.1 per cent from Origin Energy. Experts are concerned that household prices in SA are set to be the highest in the world, putting immense pressure on the household budget.

In today’s ever-increasing energy market, it is important to get to know your energy usage. Edge’s tips for residential and small to medium business customers are:

Understand your consumption. E.g. Do you need smart metering?

Are you on the right tariff? Changing tariffs could save you hundreds of dollars per year.

Shop around. There are a number of retailers offering discounts of varying levels. It’s important you are comparing apples with apples.

If you’re a small to medium business and want to take a proactive approach to your electricity contracts, contact Edge Utilities here.

Edge Utilities is the online service arm of Edge Energy Services helping SME leverage the strength, experience and influence of our energy experts.

A joint statement issued by Queensland Treasurer Curtis Pitt and Queensland Energy Minister Mark Bailey in early June announced that the Swanbank E Power Station (385 MW) would be recommissioned in the first quarter of 2018. Bringing the gas-powered station back online is part of a multi-faceted approach by the government to increase supply and reduce volatility in the energy market.

Stanwell Corporation withdrew Swanbank E from operation in late 2014 due to an over-supply of generation. Since then, Stanwell has been selling their gas to LNG exporters and the Brisbane Short Term Trading Market (STTM). Once back in operation Stanwell will no longer do this because the gas will be consumed by the power station. This will reduce the overall volumes sold to LNG exporters and the STTM. It is important to note that the Brisbane STTM is where gas powered generators buy gas from, particularly in periods of high electricity demand.

It will remain to be seen how effective the increased supply of electricity will be, considering the increased competition for gas in the Queensland market. If more gas becomes available from either increased gas production or government -imposed export restrictions, then we are likely to see prices and volatility reduce. Alternatively, the implications are likely to be modest if more gas isn’t made available.

A statement released yesterday by the Queensland Government outlines its plan to put downward pressure on energy prices, generate jobs, and invest in renewables infrastructure.

The Queensland Premier, Treasurer, and Energy Minister jointly promoted the “Powering Queensland Plan” which will see the government invest $1.16 billion to ensure affordable, secure and sustainable energy supply for homes and businesses.

The plan shows several ways the government will put downward pressure on electricity prices. In the longer term, this includes:

Reverse Auction of 400 MW of renewable energy including 100 MW of energy storage

Improve project facilitation, planning, and network connections

Implement an action plan on gas including purchasing gas fields

Deliver a plan to improve generation in North Queensland

In the short term the plan will:

Invest $770m to cover the cost of the Solar Bonus Scheme

Restart Swanbank E power station

Direct Stanwell to undertake strategies to place downward pressure on wholesale price

Swanbank E is a 385 MW combined cycle gas turbine which was put into long term care-and-maintenance (cold storage) in 2014 due to the market being over-supplied with generation. A previous statement from Stanwell had announced it would be back online at the end of 2018 if Stanwell determined it was required.

In addition to restarting the Swanbank E power station, the government will also direct Stanwell to undertake strategies to place downward pressure on wholesale prices. Stanwell is a large generation corporation which owns 3,689 MW of mainly baseload generation. This is without the additional capacity that Swanbank E will provide.

With the full details of the ‘Powering Queensland Plan’ delivered yesterday, there was immediate market movement.

The market reacted by reducing prices across the forward periods but particularly in the near term.

Queensland recorded the greatest reduction with a drop of $10.43/MWh followed by New South Wales which reduced $5.19/MWh. Victorian prices also reduced $3.40/MWh showing the importance of baseload generation in the current market.

If your business needs certainty around energy prices, please contact us on 07 3232 1115 to speak to one of our Senior Portfolio Managers.

A severe heatwave in South Australia yesterday culminated in increased usage that pushed demand beyond the capabilities of the generators. This led to outages in the network as the market operator commenced load shedding.

Demand was the highest it had been for three years with the maximum five-minute demand set at 3077.47MW at 6:15 p.m. market time. This is despite a continued uptake of residential solar photovoltaic (PV) systems.

There were some interesting announcements leading into the period. The Australian Energy Market Operator (AEMO) was aware this was an unusual event and published a market notice at 3:15 p.m. (market time) to be aware that temperatures would be high across SA, NSW and QLD.

There were concerns surrounding reserves for SA most of the day. AEMO operates with three Lack-of-Reserve (LOR) levels.

LOR1: If the largest unit fails there will be a LOR2 condition

LOR2: If the largest unit fails, there will be a loss of power

LOR3: There is an actual loss of power. There is no solution in which all demand can be met

There were several LOR1 conditions during the day but AEMO didn’t respond. More interestingly was a LOR2 warning at 5:13 p.m. (market time) stating that AEMO was aware of an actual LOR2 condition forecast until 7:00 p.m. (market time). Required contingency was 200 MW but there was only 114 MW available. AEMO decided not to intervene but wanted to seek a market response. As we now know, the LOR2 turned into an LOR3 as wind generation reduced.

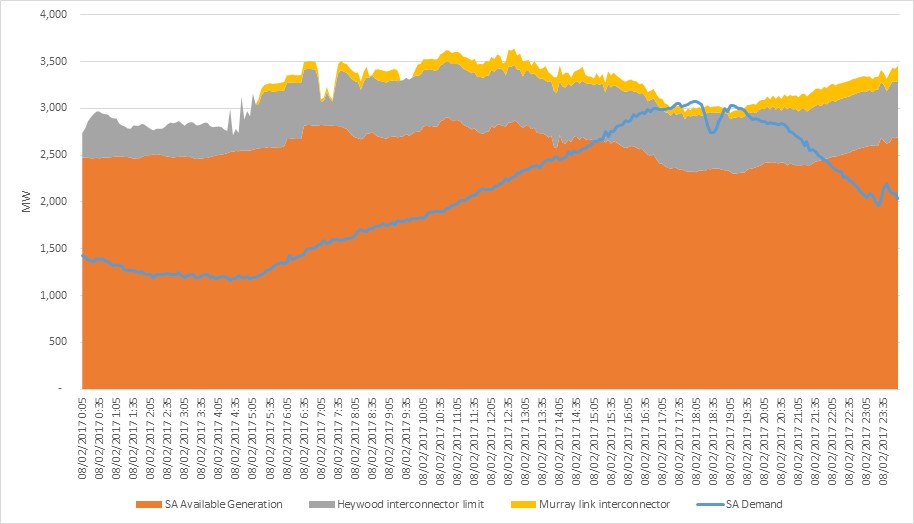

Figure 1: SA Generation and Demand 08/02/2017

The orange area represents the available generation for the state with the grey and yellow being the maximum support from the interconnector. The blue line is SA (five-minute) demand. The heat didn’t dissipate as the day wore on. Electricity demand continued to rise with the addition of domestic air conditioners as residents were returning home. The drop in the orange availability represents the reduction in wind. As wind kept reducing in capacity, there was insufficient power in the state to meet demand and there were rolling brown-outs.

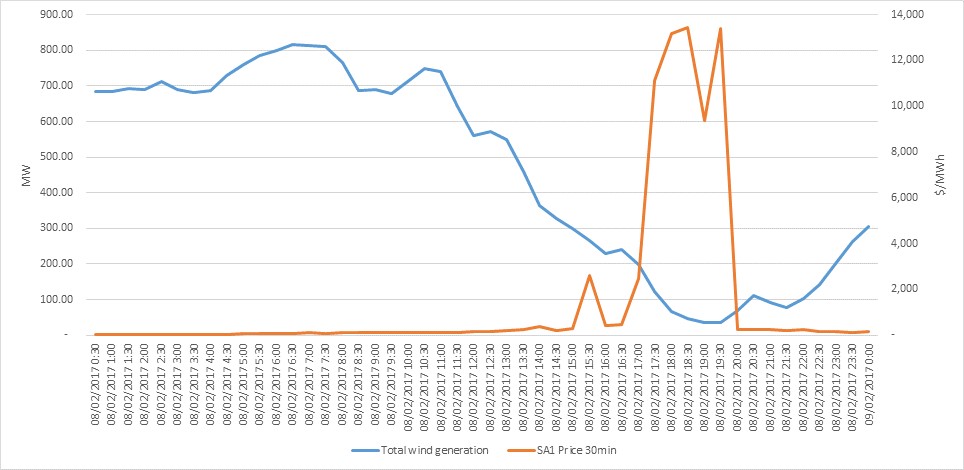

Figure 2: SA wind generation and spot prices 08/02/2017

The 30-minute wind generation data shows the drop in availability. Wind generation is affected during hot weather as there isn’t enough energy in warm wind.

There are wide reports that additional power stations were available but didn’t run. Torrens Island A and Pelican Point each had a unit which was not available. It is unlikely there was enough gas going to the power stations to start another unit.

It is very questionable what market response AEMO was expecting at 5:13 p.m. since all available generators were on (except one unit at Pelican Point and one at Torrens Island A). From the outside, it looks like they were hoping LOR2 would not become LOR3.

With temperatures forecast at similar levels today, more outages can be expected. With the political backlash, it is unlikely there would be an appetite to curtail residential customers again. This could mean that AEMO and the Government may prefer to take the risk with business and commercial customers instead.

If you’re looking for stability in your energy pricing, please contact our energy procurement experts here or on 07 3232 1115.

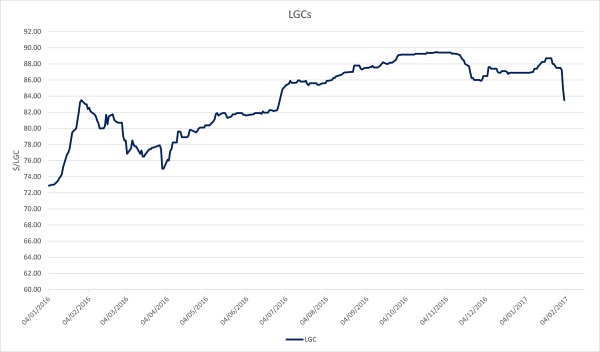

Yesterday we considered the possibility of large-scale generation certificate (LGCs) prices reducing due to the federal review. Prices have slid $4/certificate this week.

In recent news reports, ERM founder, Trevor St Baker said the government would need to adjust the renewable energy target (RET) to 20,000 gigawatt hours to fall in line with infrastructure expectations.

“There is no way we are going to make the 33,000 target. It’s impossible to get there.” Mr St Baker said.

We concur, and have for quite some time. Fundamentally, in a politically stable environment, we can only see LGC prices trending to and sitting at the full tax adjusted penalty of around $93/LGC. There aren’t enough certificates in the market to fulfil obligations without a sharp increase in the number of new renewable generation projects coming online over the next two years. We still forecast an LGC deficit during 2018.

However, we do not live in a politically stable environment. Abbott and Turnbull went head to head last week over the future of the RET. This combined with 2016 liabilities being squared away, has seen $4/certificate shaved off spot LGC prices this week. This is a reduction of approximately 5 percent. The movement shows how quickly environmental markets can change when politicians weigh-in.

After almost guaranteed price increases following the bipartisan agreement in 2015, trade for 2017 just got interesting.