At the end of the last week, AEMO flagged the possibility of extreme temperatures for the following week in South Australia, Victoria and New South Wales.

Weather forecasts were showing a large uncertainty in the predicted temperatures. Predictions ranged from mid to high 30s for Victoria, low to mid 40s for South Australia and high 30s for New South Wales. The key risk in these forecasts was the possibility of temperatures exceeding 40 degrees in two or more regions simultaneously.

On 11 January, AEMO published a market notice highlighting the forecast extreme temperatures in South Australia and elevated temperatures in Victoria and New South Wales. In this notice, AEMO provided forecast temperatures and generation capacity reference temperatures for generators to consider when updating their generation levels. Temperature and humidity have significant impacts on the performance of coal and gas powered generation.

On the back of this, AEMO updated its demand forecast and the resulting higher demand caused a lack of reserve to be triggered. The lack of reserve was forecast between 15:00 and 18:00 on 15 January. AEMO requested a market response from generators to make generation available to fulfil the shortfall.

Between 11 January and 15 January AEMO published further market notices updating the expected lack of reserve for 15 January and requested further generation response.

Pre-dispatch prices and demand for 15 January were published by AEMO the day prior. Spot prices were forecast to reach $14,500/MWh based on a demand of 8,800MW, which is significantly higher than normal levels.

As the afternoon approached, temperatures were high but a cool change was also approaching.

At 11:57 on 15 January, AEMO issued a market notice cancelling the lack of reserve.

As a result of the increased availability of generators and the cool change, AEMO revised their demand forecast down 800MWs. The resultant shift in supply and demand drove forecast prices down from $14,500 /MWh to $300/MWh.

Contract market prices are influenced by the outcomes of the spot market. As a result of the forecast high prices in South Australia,Victoria and New South Wales, the contract market prices increased in the build-up to 15 January; however, as the forecast spot prices and actual spot prices reduced, the contract market also reduced.

Retailers and large industrials are provided cover from the volatility of the spot market by purchasing contracts at a fixed price. However, the impact of the spot market can influence when volume is purchased to achieve the desired outcome for a business.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The COAG Energy Council met today for their 21st meeting. On the agenda was AEMO addressing their work in preparing the grid for summer, bringing down electricity costs and ensuring long term grid reliability and security.

AEMO highlighted the priority of work being undertaken to ensure that there is enough dispatchable generation in the NEM and integration of renewable and distributed energy resources. The Ministers agreed to a work program for the ESB to develop advice on a long term, fit for purpose market framework to support reliability that could apply from the mid-2020s. There was very little detail on this framework, however Edge will look to discover more.

Reliability

Ministers agreed to the final draft bill which gives effect to the Retail Reliability Obligation. The final package of rules will be brought to Council for approval in the first half of 2019, with a target commencement date of 1 July 2019.

Transmission upgrades

Ministers agreed on an approach to deliver the Group 1 transmission network projects. Group 1 projects include:

• Increasing transfer capacity between New South Wales, Queensland, and Victoria by 170-460 MW;

• Reducing congestion for existing and committed renewable energy developments in western and north-western Victoria; and

• Remedy system strength in South Australia.

In the Base plan, these initial transmission developments for Group 1 are costed at between $450 million and $650 million, and the assets will continue to benefit consumers well beyond the 20-year ISP forecast period. More cost benefit analysis work is to be conducted on Group 2 and 3 projects.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

RCR Tomlinson entering voluntary administration this week has been a major eye-opener in the renewable energy world. The engineering firm had shown signs of stress earlier in the year, particularly when it was forced to record a $57 million write-down on the value of it’s Daydream and Hayman solar farms in Queensland. Following this, the company successfully went to market and raised an additional $100 million in capital. Now after incurring liquidated damages as a result of running late on solar projects, directors had no choice but to put the company into administration.

In the renewable energy space, these events particularly emphasise the potential risk of entering into a PPA with a project that requires development prior to receiving any MWh. For those considering entering into a renewable PPA, it is imperative to be mindful of the gravity of the project risk taken with these developments. With increasingly stringent connection criteria being enforced by AEMO and transmission companies, corporate PPA off-takers need to consider the structuring of risk in the PPA to avoid being exposed in situations like this.

There are several ways to manage project risk through legal and commercial arrangements. Without being privy to the details of RCR Tomlinson’s contracts, it would appear that the company was wearing “connection to the grid” risk. On face value, this would have felt like a win to the off-taker. However, the off-takers are now in a position where the risk has fallen onto them due the collapse of the company. Whilst RCR Tomlinson shouldn’t have taken that risk, the PPA counterparties arguably also should not have turned a blind eye to the potential project risk.

This is an important lesson for any corporate entity looking to enter into a PPA, by understanding whether your developer and construction partners have the appropriate means to manage the risk that is placed on them. Having liquidated damages in a contract is essential. However, be mindful that at the end of the day, if a company is placed into administration and subsequently liquidated, liquidated damages are worthless.

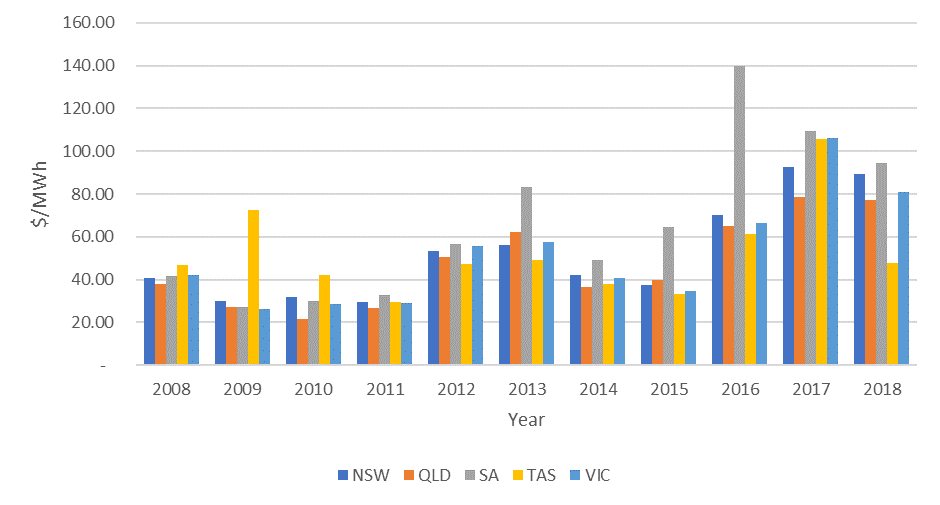

The electricity spot prices were generally higher for the winter period (June to August) than the preceding three months. The largest contributing factors were higher gas prices and increased demand for most of the regions. This excludes Tasmania where average prices fell from $80.26/MWh in autumn to $47.55/MWh in winter. Demand was still higher in the Tasmanian region, however additional rain meant that many of the hydro plants were running, as opposed to spilling water without generating. This put downwards pressure on the local prices.

The lower Tasmanian prices didn’t result in lower prices for the rest of the National Electricity Market (NEM). Across all regions, the prices during the 2018 winter were lower than the 2017 winter, however were still very high in a historical context. Looking back across the last 10 winters, the previous two (three for South Australia where Northern Power Station closed in May 2016) look like outliers. In fact, averaging the previous 8 years from 2008 to 2016, prices have been lower for all regions.

Figure 1: Historical prices for winter

It should be noted that prices in both 2012 and 2013 were affected by a carbon tax, which was subsequently repealed in 2014. Since then, there has been a steady price increase in all mainland NEM regions. The prices appear to have plateaued, however not reduced. In Queensland, the Government provided a direction to Stanwell Corporation to adopt strategies to reduce wholesale prices. Since the direction, there have been fewer price spikes (prices above $300/MWh). Although, the prices outside summer months are not reducing. Queensland is the only NEM region which had lower demand during winter compared to autumn. Price spikes in June caused by issues on the transmission network and lower availability at the start of winter kept average prices higher.

New South Wales had the same transmission issues as Queensland, and rolling planned outages at coal fired power stations meant that there was little spare base load capacity available. Victoria had high overall prices with few price spikes and was the only NEM region which didn’t have any prices above $350/MWh. Higher demand and gas prices kept overall prices high in the region. With lower availability in New South Wales, Victoria exported an average of 389 MW into the region compared to 57 MW during autumn. South Australia is heavily dependent on gas powered generation when there is insufficient renewable generation to power the state. This makes South Australia vulnerable to higher demand and higher gas prices, both of which were prevalent during winter. Prices were the lowest in three years, however still the highest of any NEM region. There is still a large amount of domestic gas usage in South Australia which means that prices tend to spike during winter. This occurred again in 2018.

The market didn’t run completely smoothly during the winter period. On Saturday 25 August 2018, multiple simultaneous lightning strikes on critical infrastructure caused load shedding. The lightning strikes occurred on the border between New South Wales and Queensland causing a loss of the main interconnector between these two regions. At the time, Queensland was supplying New South Wales with generation. The sudden loss of generation from Queensland caused load to be tripped in New South Wales. The loss of frequency also triggered a shutdown of the interconnection between South Australia and Victoria for reasons still being investigated by AEMO. This caused load shedding in Victoria and Tasmania. In total, 800 MW of load was lost in New South Wales, 280 MW in Victoria and 80 MW in Tasmania. This was predominantly industrial load which was reconnected within an hour.

Higher spot prices and concerns over the stability of the grid has caused the forward prices to increase. Snowy Hydro continued to draw down on its dam levels and with a dry outlook, the inflows could be lower than previous years. If Snowy Hydro reduces their output during 2019, spot prices could be even higher than current prices.

We are also seeing a separation between prices again. Though there were increases across all states, these were highest in Victoria ($16.56/MWh) and New South Wales ($15.88/MWh), and lowest in Queensland ($7.38/MWh).

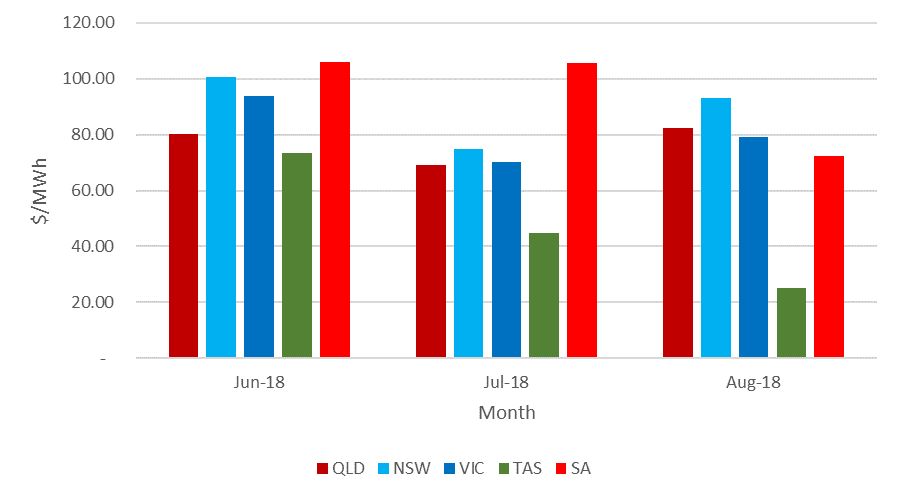

Figure 3: Calendar year 2019 forward contracts

NSW

QLD

SA

VIC

01-Jun-18

68.18

62.53

87.00

74.00

31-Aug-18

84.06

69.91

96.09

90.56

Source: ASX

There continues to be additional generation added to the market, mainly renewable energy. Going forward, it will be the integration of this renewable energy into the market which will ultimately determine if prices will reduce or if a more volatile market will be created. It is certainly unlikely in the near term that spot prices will return to historical levels (where the cost of energy during winter was in the $30s/MWh).

Looking forward

Q119 continues to be a period of concern across the market, as market participants continue to accept higher prices for swaps in the interest of reducing or removing exposure to spot prices. The BOM is forecasting hot and dry temperatures during the period, which are conditions that tend to cause volatile and higher spot prices.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Energy Analyst, Nick Clark on 07 3905 9227 or on 1800 EDGE ENERGY.

In late 2017, the Energy Security Board (ESB) developed a scheme to provide investment certainty in the electricity market, which would address Australia’s commitments under the Paris Agreement.

The Coalition had ruled out a carbon tax, other cap-and-trade schemes and virtually any other scheme which had been attempted in the past. This left very few options for the ESB to appropriately address investment certainty in the electricity market. The ESB eventually developed an innovative scheme called the National Energy Guarantee (NEG). The basis of the NEG was essentially a cap-and-trade scheme for environmental certificates and, as a sweetener, it also had a reliability obligation. Essentially, the scheme was linked to contracts with retailers to make it sound like it wasn’t a cap-and-trade scheme. The reliability obligation would force retailers to purchase firm contracts if there was a reliability gap. The additional demand for firm contracts was thought to increase demand for firm generation.

The Australian Labor Party (ALP) was willing to support the NEG on the assumption that they would be able to increase the target for carbon reduction. The states were also largely on-board, on the basis that state-based schemes could continue under the NEG.

The new focus of the Federal Government will be reducing prices in the energy sector.

Prior to the legislation being enacted, Malcolm Turnbull was removed as Prime Minister. Even though Scott Morrison, the succeeding Prime Minister of Australia, had previously been supportive of the NEG, he conceded that it would no longer be acceptable to his party and declared the NEG dead. At the same time, the Australian Competition and Consumer Commission delivered a paper suggesting ways of reducing electricity prices. The new Energy Minister, Angus Taylor, was nicknamed the “Minister for Bringing Prices Down” declaring the new focus for the Federal Government in the energy sector.

Subsequently, the ALP has been quietly arguing for bipartisan support to potentially revisit the NEG in its entirety. Recently, Mr Morrison has been open to the reliability portion of the NEG being resurrected. Mr Morrison has expressed interest in meeting with the states and territories to discuss the possibility of legislating the reliability aspect of the NEG on its own.

While the NEG is still a topic of conversation in parliament, it seems that only the reliability obligation may survive.

As a whole, energy policy is shaping up to be a key differential in the next Federal election. In the meantime, we are seeing renewable projects going ahead across the entire system. Australia is well on track to meet and exceed the current 2020 target of 33,000 GWh of renewable energy across Australia. New investors in Australia are coming to terms with political instability, instead focusing on setting projects up directly with businesses that are considering their own schemes due to the lack of political leadership shown in Parliament.

As we come towards the end of 2018, the outlook is grim for bipartisan support of long-term energy policy; however, we may still have a way forward as consumers start to forge ahead of the political vacuum. The Federal government has warned against businesses forming a technocracy to effectively create laws, however given the failure of the government to provide an alternative, this may be the way that policies will be formed going forward.

In a media statement released 30 August, the Queensland Government confirmed their intention to establish CleanCo, Queensland’s third publicly owned electricity generator. CleanCo will have a strategic portfolio of low and no emission power generations assets, and will build, own and operate new renewable generation. It is understood that CleanCo will take control of assets including Wivenhoe, Barron Gorge and Kareeya hydro power stations and the Swanbank E gas power station, courtesy of a restructure of the two current publicly-owned electricity generators – CS Energy and Stanwell Corporation. CleanCo is expected to be trading by mid-2019.

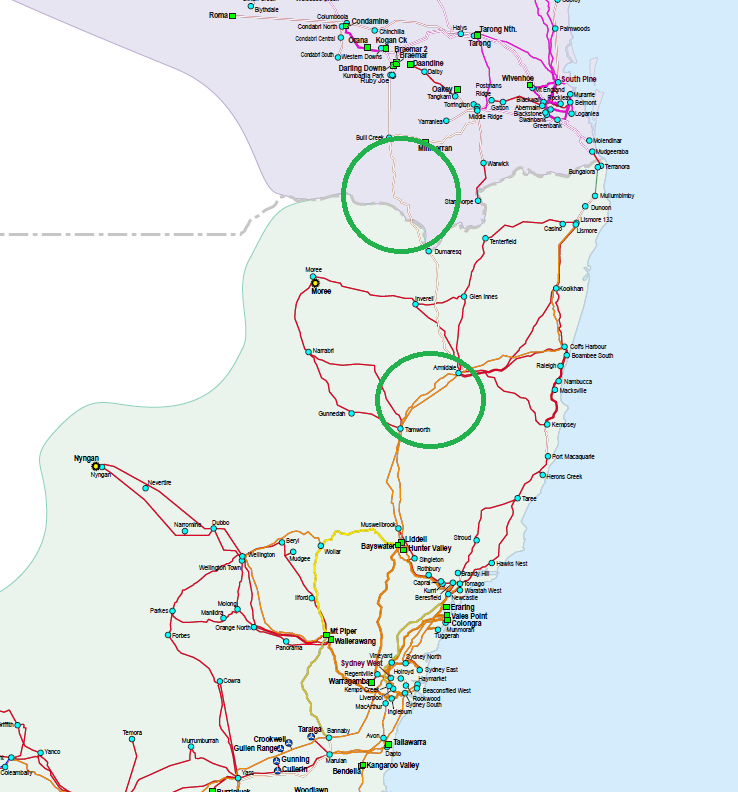

On Saturday, two critical lines connecting Queensland to the rest of the National Electricity Market (NEM) were lost resulting in load shedding. In total, New South Wales shed 800 MW of load, Victoria 280 MW and 80 MW in Tasmania. This was predominately industrial load which was reconnected within an hour. Lightning is the most likely cause.

While farmers in Northern New South Wales and Southern Queensland were celebrating much needed rain, the transmissions lines between Bulli Creek and Dumaresq tripped off. At the same time, the line was lost between Armidale and Tamworth in Northern New South Wales. At the same time, South Australia was separated from Victoria. Refer to image below for map reference.

Source: AEMO

AEMO is still investigating the causes, however there is likely to be issues regarding frequency response capabilities as this is limited in region.

AEMO expects to release a full report once they have all the necessary information. At this stage, they are not expecting further loss of load.

If you have any questions regarding the event, call Edge on 07 3905 9220 or 1800 334 336.

The Prime Minister Malcolm Turnbull has, once again, made last minute changes to the National Energy Guarantee (NEG).

When the states threatened to walk away from the NEG, Mr Turnbull responded by making the emissions target regulated rather than legislated. This means that a minister is able to change the target without the support of the parliament. Over the weekend, Mr Turnbull came under pressure internally with several backbenchers, led by former Prime Minister Tony Abbott, wanting to get rid of the targets all together.

A number of changes to the NEG were announced on Monday 20 August, 2018. These changes include providing additional controversial powers to the ACCC where they will have the ability to:

Force power stations to stay online; and

Force divestment of companies.

Mr Turnbull also reverted to making the emissions target a legislated target, however conceded that the current parliament was unlikely to agree on a target. Mr Turnbull has urged for the NEG to go ahead with an emissions target being set some time in the future once there is a possibility of agreement.

The centrepiece of the NEG was supposed to be certainty. If the current Government is unable to set an initial target even at the current international commitment, it is difficult to see investment flowing from the NEG. The additional powers of market intervention will also be looked on very sceptically from the outside. ACCC was opposed to AGL buying generation in New South Wales and now they may get a vehicle for forcing a divestment.

In the short term, it is unlikely that Labor will want to agree on the NEG or anything else which will put this to rest as the political fallout continues for the Coalition.

If you would like to know more about the NEG, call Edge on 1800 334 336 or 07 3905 9226.

Yesterday the COAG Energy Council released a draft of the proposed changes to the National Electricity Law that would implement the National Energy Guarantee (NEG).

The draft Bill sets out:

Who is liable under the emissions reduction and reliability requirements;

The key aspects of the emissions and reliability requirements;

The compliance and penalty framework;

The additional functions and powers of the Australian Energy Market Commission (AEMC), the Australian Energy Regulator (AER), and the Australian Energy Market Operator (AEMO) to support the implementation of the Guarantee; and

A new emissions objective, applicable to the emissions requirement, to guide rule-making by the AEMC and the exercise of related functions and powers by the AEMC, AEMO and AER.

Stakeholders are encouraged to make written submissions on the draft Bill by 12 September, 2018. Submissions will be published on the COAG Energy Council’s website, following a review of claims for confidentiality.

If you would like further information please get in contact with your Portfolio Manager or follow this link to the COAG Energy Council website.

The Council of Australian Governments (COAG) meeting has ended and the Federal Energy Minister Josh Frydenberg will be able to move the National Energy Guarantee (NEG) to the next stage.

The next stage will involve taking the legislation to the Coalition party room on Tuesday. If the party room agrees with the draft legislation, there will be a teleconference with COAG and the draft legislation will be released for public consultation.

Minister Frydenberg still believes that legislation will pass in 2018 for a 2020 start. Federal Labor, the two Labor held states (Victoria and Queensland) as well as the Australian Capital Territory are still sceptical. Particularly, Victoria has concerns that the NEG doesn’t seem to support lower power bills, emissions reduction and more renewable energy jobs for the state.

Further details are expected to be made available on Tuesday.

If you would like to know more about the NEG, call Edge on 07 3905 9220 or 1800 334 336 or speak with your Edge Portfolio Manager.